UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

|

x |

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended June 30, 2009

|

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _________ to _________

Commission File Number: 000-21467

PACIFIC ETHANOL, INC.

(Exact name of registrant as specified in its charter)

|

Delaware

(State or other jurisdiction

of incorporation or organization) |

41-2170618

(I.R.S. Employer

Identification No.) |

| |

|

|

400 Capitol Mall, Suite 2060, Sacramento, California

(Address of principal executive offices) |

95814

(zip code) |

(916) 403-2123

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements

for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter periods that the registrant was required to

submit and post such files). Yes o No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2

of the Exchange Act.

|

Large accelerated filer o |

Accelerated filer þ |

|

Non-accelerated filer o (Do not check if a smaller reporting company) |

Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No þ

As of August 7, 2009, there were 57,644,585 shares of Pacific Ethanol, Inc. common stock, $0.001 par value per share, outstanding.

PART I

FINANCIAL INFORMATION

| |

|

|

Page |

|

Item 1. |

Financial Statements. |

|

|

| |

Consolidated Balance Sheets as of June 30, 2009 (unaudited) and December 31, 2008 |

|

F-1 |

| |

Consolidated Statements of Operations for the Three and Six Months Ended June 30, 2009 and 2008 (unaudited) |

|

F-3 |

| |

Consolidated Statements of Comprehensive Loss for the Three and Six Months Ended June 30, 2009 and 2008 (unaudited) |

|

F-4 |

| |

Consolidated Statements of Cash Flows for the Three and Six Months Ended June 30, 2009 and 2008 (unaudiated) |

|

F-5 |

| |

Notes to Consolidated Financial Statements (unaudited) |

|

F-7 |

|

Item 2. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations. |

|

2 |

|

Item 3. |

Quantitative and Qualitative Disclosures About Market Risk. |

|

12 |

|

Item 4. |

Controls and Procedures. |

|

14 |

|

Item 4T. |

Controls and Procedures. |

|

14 |

| |

|

|

|

|

PART II

OTHER INFORMATION |

| |

|

|

|

|

Item 1. |

Legal Proceedings. |

|

15 |

|

Item 1A. |

Risk Factors. |

|

16 |

|

Item 2. |

Unregistered Sales of Equity Securities and Use of Proceeds. |

|

17 |

|

Item 3. |

Defaults Upon Senior Securities. |

|

18 |

|

Item 4. |

Submission of Matters to a Vote of Security Holders. |

|

19 |

|

Item 5. |

Other Information. |

|

19 |

|

Item 6. |

Exhibits. |

|

19 |

|

Signatures |

|

|

20 |

| |

|

|

|

| Exhibits Filed with this Report |

|

|

PART I - FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS.

PACIFIC ETHANOL, INC.

CONSOLIDATED BALANCE SHEETS

(in thousands)

| |

|

June 30, |

|

|

December 31, |

|

|

ASSETS |

|

|

|

|

|

|

| |

|

(unaudited) |

|

|

* |

|

|

Current Assets: |

|

|

|

|

|

|

|

|

Cash and cash equivalents |

|

$ |

12,073 |

|

|

$ |

11,466 |

|

|

Investments in marketable securities |

|

|

101 |

|

|

|

7,780 |

|

|

Accounts receivable, net (net of allowance for doubtful accounts of $2,270 and $2,210, respectively) |

|

|

10,175 |

|

|

|

23,823 |

|

|

Restricted cash |

|

|

— |

|

|

|

2,520 |

|

|

Inventories |

|

|

12,799 |

|

|

|

18,408 |

|

|

Prepaid expenses |

|

|

491 |

|

|

|

2,279 |

|

|

Prepaid inventory |

|

|

1,771 |

|

|

|

2,016 |

|

|

Other current assets |

|

|

2,186 |

|

|

|

3,599 |

|

|

Total current assets |

|

|

39,596 |

|

|

|

71,891 |

|

|

Property and equipment, net |

|

|

513,293 |

|

|

|

530,037 |

|

|

Other Assets: |

|

|

|

|

|

|

|

|

|

Intangible assets, net |

|

|

5,393 |

|

|

|

5,630 |

|

|

Other assets |

|

|

1,131 |

|

|

|

9,276 |

|

|

Total other assets |

|

|

6,524 |

|

|

|

14,906 |

|

|

Total Assets |

|

$ |

559,413 |

|

|

$ |

616,834 |

|

_______________

* Amounts derived from the audited financial statements for the year ended December 31, 2008.

See accompanying notes to consolidated financial statements.

PACIFIC ETHANOL, INC.

CONSOLIDATED BALANCE SHEETS (CONTINUED)

(in thousands, except par value and shares)

| |

|

June 30, |

|

|

December 31, |

|

|

LIABILITIES AND STOCKHOLDERS’ EQUITY |

|

|

|

|

|

|

| |

|

(unaudited) |

|

|

|

* |

|

|

Current Liabilities: |

|

|

|

|

|

|

|

|

Accounts payable – trade |

|

$ |

5,472 |

|

|

$ |

14,034 |

|

|

Accrued liabilities |

|

|

5,724 |

|

|

|

12,334 |

|

|

Accounts payable and accrued liabilities – construction-related |

|

|

16,761 |

|

|

|

20,304 |

|

|

Other liabilities – related parties |

|

|

2,098 |

|

|

|

608 |

|

|

Current portion – long-term notes payable (including $33,500 and $31,500, respectively due to related parties) |

|

|

62,255 |

|

|

|

291,925 |

|

|

Derivative instruments |

|

|

1,095 |

|

|

|

7,504 |

|

|

Total current liabilities |

|

|

93,405 |

|

|

|

346,709 |

|

| |

|

|

|

|

|

|

|

|

|

Notes payable, net of current portion |

|

|

13,538 |

|

|

|

14,432 |

|

|

Other liabilities |

|

|

1,954 |

|

|

|

3,497 |

|

|

Liabilities subject to compromise (Note 9) |

|

|

252,879 |

|

|

|

— |

|

|

Total Liabilities |

|

|

361,776 |

|

|

|

364,638 |

|

| |

|

|

|

|

|

|

|

|

|

Commitments and Contingencies (Notes 1 and 10) |

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

Stockholders’ Equity: |

|

|

|

|

|

|

|

|

|

Pacific Ethanol, Inc. Stockholders’ Equity: |

|

|

|

|

|

|

|

|

|

Preferred stock, $0.001 par value; 10,000,000 shares authorized; Series A: 7,000,000 shares authorized; 0 shares issued and outstanding

as of June 30, 2009 and December 31, 2008;

Series B: 3,000,000 shares authorized; 2,346,152 shares issued and outstanding as of June 30, 2009 and December 31, 2008 |

|

|

2 |

|

|

|

2 |

|

|

Common stock, $0.001 par value; 100,000,000 shares authorized; 57,644,585 and 57,750,319 shares issued and outstanding as of

June 30, 2009 and December 31, 2008, respectively |

|

|

58 |

|

|

|

58 |

|

|

Additional paid-in capital |

|

|

480,064 |

|

|

|

479,034 |

|

|

Accumulated deficit |

|

|

(322,625 |

) |

|

|

(269,721 |

) |

|

Total Pacific Ethanol, Inc. Stockholders’ Equity |

|

|

157,499 |

|

|

|

209,373 |

|

|

Noncontrolling interest in variable interest entity |

|

|

40,138 |

|

|

|

42,823 |

|

|

Total Stockholders’ Equity |

|

|

197,637 |

|

|

|

252,196 |

|

|

Total Liabilities and Stockholders’ Equity |

|

$ |

559,413 |

|

|

$ |

616,834 |

|

_______________

* Amounts derived from the audited financial statements for the year ended December 31, 2008.

See accompanying notes to consolidated financial statements.

PACIFIC ETHANOL, INC.

CONSOLIDATED STATEMENTS OF OPERATIONS

(unaudited, in thousands, except per share data)

| |

|

Three Months Ended

June 30, |

|

|

Six Months Ended

June 30, |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

Net sales |

|

$ |

70,114 |

|

|

$ |

197,974 |

|

|

$ |

156,796 |

|

|

$ |

359,509 |

|

|

Cost of goods sold |

|

|

77,935 |

|

|

|

197,531 |

|

|

|

175,703 |

|

|

|

343,408 |

|

|

Gross profit (loss) |

|

|

(7,821 |

) |

|

|

443 |

|

|

|

(18,907 |

) |

|

|

16,101 |

|

|

Selling, general and administrative expenses |

|

|

6,254 |

|

|

|

7,678 |

|

|

|

13,928 |

|

|

|

17,544 |

|

|

Goodwill impairment |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

87,047 |

|

|

Loss from operations |

|

|

(14,075 |

) |

|

|

(7,235 |

) |

|

|

(32,835 |

) |

|

|

(88,490 |

) |

|

Other income (expense), net |

|

|

(4,734 |

) |

|

|

889 |

|

|

|

(11,705 |

) |

|

|

(1,410 |

) |

|

Loss before reorganization costs and provision for income taxes |

|

|

(18,809 |

) |

|

|

(6,346 |

) |

|

|

(44,540 |

) |

|

|

(89,900 |

) |

|

Reorganization costs |

|

|

9,462 |

|

|

|

— |

|

|

|

9,462 |

|

|

|

— |

|

|

Provision for income taxes |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

Net loss |

|

|

(28,271 |

) |

|

|

(6,346 |

) |

|

|

(54,002 |

) |

|

|

(89,900 |

) |

|

Net income (loss) attributed to noncontrolling interest in variable interest entity |

|

|

(903 |

) |

|

|

1,987 |

|

|

|

(2,686 |

) |

|

|

(46,416 |

) |

|

Net loss attributed to Pacific Ethanol, Inc. |

|

$ |

(27,368 |

) |

|

$ |

(8,333 |

) |

|

$ |

(51,316 |

) |

|

$ |

(43,484 |

) |

|

Preferred stock dividends |

|

$ |

(798 |

) |

|

$ |

(1,388 |

) |

|

$ |

(1,588 |

) |

|

$ |

(2,489 |

) |

|

Deemed dividend on preferred stock |

|

|

— |

|

|

|

(761 |

) |

|

|

— |

|

|

|

(761 |

) |

|

Loss available to common stockholders |

|

$ |

(28,166 |

) |

|

$ |

(10,482 |

) |

|

$ |

(52,904 |

) |

|

$ |

(46,734 |

) |

|

Net loss per share, basic and diluted |

|

$ |

(0.49 |

) |

|

$ |

(0.23 |

) |

|

$ |

(0.93 |

) |

|

$ |

(1.08 |

) |

|

Weighted-average shares outstanding, basic and diluted |

|

|

56,985 |

|

|

|

46,455 |

|

|

|

56,999 |

|

|

|

43,254 |

|

See accompanying notes to consolidated financial statements.

PACIFIC ETHANOL, INC.

CONSOLIDATED STATEMENTS OF COMPREHENSIVE LOSS

(unaudited, in thousands)

| |

|

Three Months Ended

June 30, |

|

|

Six Months Ended

June 30, |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

Net loss |

|

$ |

(28,271 |

) |

|

$ |

(6,346 |

) |

|

$ |

(54,002 |

) |

|

$ |

(89,900 |

) |

|

Other comprehensive loss, net of tax: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net change in the fair value of derivatives |

|

|

— |

|

|

|

4,029 |

|

|

|

— |

|

|

|

3,480 |

|

|

Comprehensive loss |

|

$ |

(28,271 |

) |

|

$ |

(2,317 |

) |

|

$ |

(54,002 |

) |

|

$ |

(86,420 |

) |

See accompanying notes to consolidated financial statements.

PACIFIC ETHANOL, INC.

CONSOLIDATED STATEMENTS OF CASH FLOWS

(unaudited, in thousands)

| |

|

Six Months Ended

June 30, |

|

| |

|

|

|

|

|

|

|

````````````Operating Activities: |

|

|

|

|

|

|

|

Net loss |

|

$ |

(54,002 |

) |

|

$ |

(89,900 |

) |

|

Adjustments to reconcile net loss to cash used in operating activities: |

|

|

|

|

|

|

|

|

|

Write off of deferred financing fees |

|

|

7,545 |

|

|

|

— |

|

|

Goodwill impairment |

|

|

— |

|

|

|

87,047 |

|

|

Depreciation and amortization of intangibles |

|

|

17,339 |

|

|

|

10,754 |

|

|

Inventory valuation |

|

|

845 |

|

|

|

— |

|

|

Amortization of deferred financing fees |

|

|

980 |

|

|

|

918 |

|

|

Non-cash compensation and consulting expense |

|

|

1,032 |

|

|

|

1,456 |

|

|

(Gain) loss on derivatives |

|

|

(2,425 |

) |

|

|

4,832 |

|

|

Bad debt expense |

|

|

64 |

|

|

|

62 |

|

|

Changes in operating assets and liabilities: |

|

|

|

|

|

|

|

|

|

Accounts receivable |

|

|

13,584 |

|

|

|

(7,832 |

) |

|

Restricted cash |

|

|

2,520 |

|

|

|

(7,569 |

) |

|

Inventories |

|

|

4,764 |

|

|

|

(19,946 |

) |

|

Prepaid expenses and other assets |

|

|

2,840 |

|

|

|

(2,941 |

) |

|

Prepaid inventory |

|

|

245 |

|

|

|

(2,436 |

) |

|

Accounts payable and accrued expenses |

|

|

(5,809 |

) |

|

|

(10,032 |

) |

|

Accounts payable, and accrued expenses-related party |

|

|

1,490 |

|

|

|

(645 |

) |

|

Net cash used in operating activities |

|

|

(8,988 |

) |

|

|

(36,232 |

) |

|

Investing Activities: |

|

|

|

|

|

|

|

|

|

Additions to property and equipment |

|

|

(1,693 |

) |

|

|

(103,692 |

) |

|

Proceeds from sales of available-for-sale investments |

|

|

7,679 |

|

|

|

11,798 |

|

|

Proceeds from sales of property and equipment |

|

|

— |

|

|

|

206 |

|

|

Net cash provided by (used in) investing activities |

|

|

5,986 |

|

|

|

(91,688 |

) |

|

Financing Activities: |

|

|

|

|

|

|

|

|

|

Proceeds from borrowing under DIP Financing |

|

|

12,278 |

|

|

|

— |

|

|

Proceeds from related party borrowing |

|

|

2,000 |

|

|

|

— |

|

|

Proceeds from all other borrowings |

|

|

— |

|

|

|

81,891 |

|

|

Net proceeds from issuance of preferred stock and warrants |

|

|

— |

|

|

|

72,167 |

|

|

Principal payments paid on borrowings |

|

|

(10,669 |

) |

|

|

(8,799 |

) |

|

Cash paid for debt issuance costs |

|

|

— |

|

|

|

(838 |

) |

|

Preferred share dividend paid |

|

|

— |

|

|

|

(2,489 |

) |

|

Dividend paid to noncontrolling interests |

|

|

— |

|

|

|

(617 |

) |

|

Net cash provided by financing activities |

|

|

3,609 |

|

|

|

141,315 |

|

|

Net increase in cash and cash equivalents |

|

|

607 |

|

|

|

13,395 |

|

|

Cash and cash equivalents at beginning of period |

|

|

11,466 |

|

|

|

5,707 |

|

|

Cash and cash equivalents at end of period |

|

$ |

12,073 |

|

|

$ |

19,102 |

|

See accompanying notes to consolidated financial statements.

PACIFIC ETHANOL, INC.

CONSOLIDATED STATEMENTS OF CASH FLOWS (CONTINUED)

(unaudited, in thousands)

|

Supplemental Information: |

|

|

|

|

|

|

|

Interest paid ($0 and $7,072 capitalized) |

|

$ |

2,176 |

|

|

$ |

8,271 |

|

|

Non-Cash Financing and Investing activities: |

|

|

|

|

|

|

|

|

|

Accrued additions to property and equipment |

|

$ |

— |

|

|

$ |

8,075 |

|

|

Preferred stock dividend declared |

|

$ |

1,588 |

|

|

$ |

— |

|

|

Deemed dividend on preferred stock |

|

$ |

— |

|

|

$ |

761 |

|

See accompanying notes to consolidated financial statements.

PACIFIC ETHANOL, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

|

1. |

ORGANIZATION AND BASIS OF PRESENTATION. |

Organization and Business – The consolidated financial statements include the accounts of Pacific Ethanol, Inc., a Delaware corporation (“Parent”), and all of its wholly-owned subsidiaries, including Pacific Ethanol

California, Inc., a California corporation, Kinergy Marketing LLC, an Oregon limited liability company (“Kinergy”) and the consolidated financial statements of Front Range Energy, LLC, a Colorado limited liability company (“Front Range”), a variable interest entity of which Pacific Ethanol, Inc. owns 42% (collectively, the “Company”).

The Company produces and sells ethanol and its co-products, including wet distillers grain (“WDG”), and provides transportation, storage and delivery of ethanol through third-party service providers in the Western United States, primarily in California, Nevada, Arizona, Oregon, Colorado, Idaho and Washington.

The Company sells ethanol to gasoline refining and distribution companies and WDG to dairy operators and animal feed distributors.

The Company’s four ethanol facilities, which produce its ethanol and co-products, are as follows:

|

Facility Name |

Facility Location |

Date Operations

Began |

Estimated Annual

Production Capacity

(gallons) |

| |

|

|

|

|

Stockton |

Stockton, CA |

September 2008 |

60,000,000 |

|

Magic Valley |

Burley, ID |

April 2008 |

60,000,000 |

|

Columbia |

Boardman, OR |

September 2007 |

40,000,000 |

|

Madera |

Madera, CA |

October 2006 |

40,000,000 |

In addition, the Company owns a 42% interest in Front Range, which owns a plant located in Windsor, Colorado, with annual production capacity of up to 50 million gallons.

Chapter 11 Filings – On May 17, 2009, five indirect wholly-owned subsidiaries of the Company, namely, Pacific Ethanol Holding Co. LLC, Pacific Ethanol Madera LLC, Pacific Ethanol Columbia, LLC, Pacific Ethanol Stockton, LLC and

Pacific Ethanol Magic Valley, LLC (collectively, the “Bankrupt Debtors”) each commenced a case by filing voluntary petitions for relief under chapter 11 of Title 11 of the United States Code (the “Bankruptcy Code”) in the United States Bankruptcy Court for the District of Delaware (the “Bankruptcy Court”) in an effort to restructure their indebtedness (“Chapter 11 Filings”).

Neither Parent nor any of its other direct or indirect subsidiaries, including Kinergy and Pacific Ag. Products, LLC (“PAP”), have filed petitions for relief under the Bankruptcy Code. The Company continues to manage the Bankrupt Debtors pursuant to an asset management agreement and Kinergy and PAP continue

to market and sell their ethanol and feed production pursuant to existing marketing agreements. The Bankrupt Debtors continue to operate their businesses as “debtors-in-possession” under jurisdiction of the Bankruptcy Court and in accordance with applicable provisions of the Bankruptcy Code and order of the Bankruptcy Court.

PACIFIC ETHANOL, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

Liquidity – The Company’s financial statements have been prepared on a going concern basis, which contemplates the realization of assets and the satisfaction of liabilities in the normal course of business. The Company believes

that it has sufficient liquidity to meet its anticipated working capital, debt service and other liquidity needs only through the end of August 2009, provided that Wachovia Capital Finance Corporation (“Wachovia”) continues to fund Kinergy’s credit facility despite an existing default, and Lyles United, LLC and Lyles Mechanical Co. do not pursue an action against the Company’s default on an aggregate of $31,500,000 of indebtedness to those entities. The Company has suspended operations

at three of its four wholly-owned ethanol production facilities due to market conditions and in an effort to conserve capital. The Company has also taken and expects to take additional steps to preserve capital and generate additional cash.

Subsequent to the Chapter 11 Filings, the Bankrupt Debtors obtained debtor-in-possession financing (“DIP Financing”) in the amount of up to $20,000,000 to fund working capital and general corporate needs, including the administrative costs of the Chapter 11 Filings. The DIP Financing provides the Bankrupt

Debtors financing to reimburse Parent for certain direct and indirect costs in accordance with an asset management agreement. The DIP Financing matures in mid-November 2009, or sooner if certain covenants are not maintained. These covenants include various reporting requirements to the lenders, as well as confirmation of a plan of reorganization prior to the maturity date. The Company believes it is in compliance with the DIP Financing covenants. As of June 30, 2009, the Bankrupt Debtors have utilized $12,278,000

of the DIP Financing. The Company believes that the remaining undrawn amount of $7,722,000 will provide enough cash to allow the Bankrupt Debtors to obtain a confirmed plan of reorganization with their secured and unsecured creditors through the maturity date.

The Bankrupt Debtors are in default under their construction-related term loans and working capital lines of credit in the aggregate amount of $246,483,000. In addition, Parent is in default under its $31,500,000 notes payable to Lyles United, LLC and Lyles Mechanical Co. In February 2009, the Company entered into forbearance

agreements with each of these lenders, which were amended in March 2009, under which the lenders agreed to forbear from exercising their rights until April 30, 2009 absent further defaults. These forbearances have not been extended.

Kinergy has renegotiated and amended its credit facility with Wachovia. Wachovia has agreed to continue providing up to $10,000,000 for Kinergy’s working capital needs. The term of the amended credit facility extends through October 2010. In addition, the amended credit facility required that Parent obtain certain

additional financing by May 31, 2009, a date that was chosen based on the Company’s then-foreseeable cash needs. This additional financing has not been obtained. Consequently, Kinergy is not in compliance with the Wachovia facility. Although Kinergy is not in compliance, Wachovia continues to fund the credit facility and has given no indication of an intention to take any action in respect of Kinergy’s noncompliance.

The Company is actively pursuing a number of alternatives, including seeking a confirmed plan of reorganization, restructuring its debt with Lyles United, LLC and Lyles Mechanical Co. and seeking to raise additional debt or equity financing, or both. There can be no assurance, however, that the Company will be successful.

If the Company cannot confirm a plan of reorganization, restructure its debt and raise sufficient capital in a timely manner, it may need to seek further protection under the U.S. Bankruptcy Code, including at the Parent level.

Except as to the Chapter 11 Filings, the consolidated financial statements do not include any other adjustments that might result from the outcome of these matters.

PACIFIC ETHANOL, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

SOP 90-7 – The American Institute of Certified Public Accountants Statement of Position 90-7, Financial Reporting by Entities in Reorganization under the Bankruptcy Code (“SOP

90-7”), which is applicable to companies in chapter 11 of the Bankruptcy Code, generally does not change the manner in which financial statements are prepared. However, among other disclosures, it does require that the financial statements for periods subsequent to the filing of the chapter 11 petition distinguish transactions and events that are directly associated with the reorganization from the ongoing operations of the business. Revenues, expenses, realized gains and losses, and provisions for losses

that can be directly associated with the reorganization and restructuring of the business must be reported separately as reorganization items in the statements of operations. The balance sheet must distinguish prepetition liabilities subject to compromise from both those prepetition liabilities that are not subject to compromise and from postpetition liabilities. Liabilities that may be affected by a plan of reorganization must be reported at the amounts expected to be allowed, even if they may be settled for

lesser amounts. In addition, reorganization items must be disclosed separately in the statement of cash flows. The Company has applied the provisions of SOP 90-7 to the Chapter 11 Filings for only the affected Bankrupt Debtors.

Contractual interest expense represents amounts due under the contractual terms of outstanding debt, including liabilities subject to compromise for which interest expense is not recognized in accordance with the provisions of SOP 90-7. The Bankrupt Debtors did not record contractual interest expense on certain unsecured

prepetition debt subject to compromise from the bankruptcy filing date. The Bankrupt Debtors are however, accruing interest on their DIP Financing and related Rollup Debt as these amounts are likely to be paid in full upon confirmation of a plan of reorganization. For the three months ended June 30, 2009, the Bankrupt Debtors recorded interest expense of approximately $3,727,000. Had the Bankrupt Debtors accrued interest on all of their liabilities subject to compromise from May 17, 2009 through June 30, 2009,

the Bankrupt Debtors’ interest expense would have been approximately $6,734,000.

Deferred financing fees are typically amortized on a straight-line basis until the date that the debt is due and payable either because of a stated maturity date or full payment of debt. In accordance with SOP 90-7, upon the Chapter 11 Filings, the Bankrupt Debtors wrote off approximately $7,545,000 of their unamortized

deferred financing fees related to their term loans and working capital lines of credit, which are reclassified as liabilities subject to compromise in the Company’s consolidated balance sheet at June 30, 2009.

Basis of Presentation–Interim Financial Statements –

The accompanying unaudited consolidated financial statements and related notes have been prepared in accordance with accounting principles generally accepted in the United States for interim financial information and the instructions to Form 10-Q and Rule 10-01 of Regulation S-X. Results for interim periods should not be considered indicative of results for a full year. These interim consolidated financial statements should be read in conjunction with the consolidated financial statements and related

notes contained in the Company’s Annual Report on Form 10-K for the year ended December 31, 2008. Except as discussed above and in Note 2 below, the accounting policies used in preparing these consolidated financial statements are the same as those described in Note 1 to the consolidated financial statements in the Company’s Annual Report on Form 10-K for the year ended December 31, 2008. In the opinion of management, all adjustments (consisting of normal recurring adjustments) considered necessary

for a fair statement of the results for interim periods have been included. All significant intercompany accounts and transactions have been eliminated in consolidation.

PACIFIC ETHANOL, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

The preparation of the consolidated financial statements in conformity with accounting principles generally accepted in the United States requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the

financial statements and the reported amounts of revenues and expenses during the reporting period. Significant estimates are required as part of determining allowance for doubtful accounts, estimated lives of property and equipment and intangibles, long-lived asset impairments, valuation allowances on deferred income taxes, and the potential outcome of future tax consequences of events recognized in the Company’s financial statements or tax returns. Actual results and outcomes may materially differ from

management’s estimates and assumptions.

Reclassifications of prior year’s data have been made to conform to 2009 classifications. Such classifications had no effect on net loss reported in the consolidated statements of operations.

|

2. |

NEW ACCOUNTING STANDARDS. |

On June 29, 2009, the Financial Accounting Standards Board (“FASB”) issued Statement of Financial Accounting Standards (“SFAS”) No. 168, The FASB Accounting Standards Codification and the Hierarchy of Generally Accepted Accounting Principles, a

replacement of FASB Statement No. 162. SFAS No. 168 establishes the FASB Accounting Standards Codification (“Codification” or “ASC”) as the complete source of authoritative U.S. Generally Accepted Accounting Principles (“GAAP”). Rules and interpretive releases of the Securities and Exchange Commission (“SEC”) under authority of federal securities laws are also sources of authoritative GAAP for SEC registrants. SFAS No. 168 is effective for financial statements

issued for interim and annual periods ending after September 15, 2009. On its effective date, the Codification will supercede all then-existing non-SEC accounting and reporting standards. The adoption of SFAS No. 168 will change the way the Company references current GAAP from referring to a particular Statement (i.e., SOP 90-7) to the related section of the Codification (i.e., ASC 852-10-45-1). As a result, the adoption of SFAS No. 168 will not have a material impact on the Company’s financial condition

or results of operations.

On May 28, 2009, the FASB issued SFAS No. 165, Subsequent Events, which provides guidance on management’s assessment of subsequent events. Historically, management had relied on U.S. auditing literature for guidance on assessing and disclosing subsequent events.

SFAS No. 165 represents the inclusion of guidance on subsequent events in the accounting literature and is directed specifically to management, since management is responsible for preparing an entity’s financial statements. SFAS No. 165 clarifies that management must evaluate, as of each reporting period, events or transactions that occur after the balance sheet date through the date that the financial statements are issued. SFAS No. 165 is effective prospectively for interim and annual financial periods

ending after June 15, 2009. The Company has adopted the provisions of SFAS No. 165 for its reporting period ending June 30, 2009. The adoption of SFAS No. 165 did not have a material impact on the Company’s financial condition or results of operations. The Company has evaluated subsequent events up through the date of the filing of this report with the SEC.

On January 1, 2009, the Company adopted SFAS No. 160, Noncontrolling Interests in Consolidated Financial Statements, an amendment to ARB No. 51. SFAS No. 160 changed the Company’s classification and reporting for its noncontrolling interests in its variable

interest entity to a component of stockholders’ equity and other changes to the format of its financial statements. Except for these changes in classification, the adoption of SFAS No. 160 did not have a material impact on the Company’s financial condition or results of operations.

PACIFIC ETHANOL, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

On January 1, 2009, the Company adopted SFAS No. 161, Disclosure about Derivative Instruments and Hedging Activities, an amendment of FASB Statement No. 133. SFAS No. 161 changed the disclosure requirements for derivative instruments and hedging activities. Entities

are required to provide enhanced disclosures about (a) how and why an entity uses derivative instruments, (b) how derivative instruments and related hedged items are accounted for under Statement No. 133 and its related interpretations and (c) how derivative instruments and related hedged items affect an entity’s financial position, financial performance and cash flows. The adoption of SFAS No. 161 resulted in enhanced disclosures and did not have any impact on the Company’s financial condition or

results of operations. (See Note 7.)

On January 1, 2009, the Company adopted Emerging Issues Task Force (“EITF”) Issue No. 07-5, Determining Whether an Instrument (or Embedded Feature) is Indexed to an Entity’s Own Stock. EITF No. 07-5 mandates a two-step process for evaluating whether

an equity-linked financial instrument or embedded feature is indexed to the entity’s own stock. The adoption of EITF No. 07-5 did not have a material impact on the Company’s financial condition or results of operations.

On January 1, 2009, the Company adopted SFAS No. 141(R), Business Combinations. SFAS No. 141(R) retains the fundamental requirements in SFAS No. 141, Business Combinations, that the acquisition method of accounting

be used for all business combinations and for an acquirer to be identified for each business combination. SFAS No. 141(R) requires an acquirer to recognize the assets acquired, the liabilities assumed, and any noncontrolling interest in the acquiree at the acquisition date, measured at their fair values as of that date, with limited exceptions specified in SFAS No. 141(R). In addition, SFAS No. 141(R) requires acquisition costs and restructuring costs that the acquirer expected but was not obligated to incur

to be recognized separately from the business combination, therefore, expensed instead of part of the purchase price allocation. SFAS No. 141(R) will be applied prospectively to business combinations for which the acquisition date is on or after January 1, 2009. The adoption of SFAS No. 141(R) did not have a material impact on the Company’s financial condition or results of operations.

In accordance with SOP 90-7, revenues, expenses, realized gains and losses, and provisions for losses that can be directly associated with the reorganization and restructuring of the business must be reported separately as reorganization items in the statements of operations. Professional fees directly related to the

reorganization include fees associated with advisors to the Bankrupt Debtors, unsecured creditors, secured creditors and administrative costs in complying with reporting rules under the Bankruptcy Code. As discussed in Note 1, the Company wrote off a portion of its unamortized deferred financing fees on the debt which is considered to be unlikely to be repaid by the Bankrupt Debtors.

The Bankrupt Debtors’ reorganization costs for the three and six months ended June 30, 2009 consist of the following (in thousands):

|

Write off of unamortized deferred financing fees |

|

$ |

7,545 |

|

|

Professional fees |

|

|

1,285 |

|

|

DIP financing fees |

|

|

600 |

|

|

Trustee fees |

|

|

32 |

|

|

Total |

|

$ |

9,462 |

|

|

4. |

MARKETABLE SECURITIES. |

The Company’s marketable securities consisted of short-term marketable securities with carrying values of $101,000 and $7,780,000 as of June 30, 2009 and December 31, 2008, respectively. As of June 30, 2009 and December 31, 2008, there were no gross unrealized gains or losses for these securities.

PACIFIC ETHANOL, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

Inventories consisted primarily of bulk ethanol, unleaded fuel and corn, and are valued at the lower-of-cost-or-market, with cost determined on a first-in, first-out basis. Inventory balances consisted of the following (in thousands):

| |

|

|

|

|

|

|

|

Raw materials |

|

$ |

6,354 |

|

|

$ |

9,000 |

|

|

Work in progress |

|

|

962 |

|

|

|

1,895 |

|

|

Finished goods |

|

|

4,016 |

|

|

|

5,994 |

|

|

Other |

|

|

1,467 |

|

|

|

1,519 |

|

|

Total |

|

$ |

12,799 |

|

|

$ |

18,408 |

|

|

6. |

PROPERTY AND EQUIPMENT. |

The ethanol industry has experienced significant adverse conditions over the course of the last 12-18 months, including prolonged negative operating margins. The Company has also experienced these adverse conditions as well as severe working capital and liquidity shortages, and in response to such conditions, the Company

has reduced its production significantly until market conditions resume to acceptable levels and working capital becomes available. The Company first reduced production in December 2008 and continued to reduce production through the first quarter of 2009. As of the end of February 2009, the Company had ceased production at its Madera, Magic Valley and Stockton facilities. The Company continues to operate its Columbia and Front Range facilities. The Company continues to assess market conditions and when appropriate,

provided it has adequate available working capital, plans to bring these facilities back to operation.

In 2008, the Company completed construction of its ethanol production facilities, with installed capacity of 220 million gallons per year, its goal since 2005. The carrying value of these facilities at June 30, 2009 was approximately $420.2 million. In accordance with the Company’s policy for evaluating impairment

of long-lived assets in accordance with SFAS No. 144, management has evaluated the facilities for possible impairment based on projected future cash flows from operations of these facilities, including the above mentioned suspensions of its facilities in the near term. Management has determined that the undiscounted cash flows from operations of these facilities over their estimated useful lives exceed their carrying values, and therefore, no impairment has been recognized at June 30, 2009. In determining future

undiscounted cash flows, the Company has made significant assumptions concerning the future viability of the ethanol industry, the future price of corn in relation to the future price of ethanol and the overall demand in relation to production and supply capacity. If the Company were required to compute the fair value in the future, it may use the work of a qualified valuation specialist who would assist it in examining replacement costs, recent transactions between third parties and cash flow that can be generated

from operations. Given the recent completion of the facilities, replacement cost would likely approximate the carrying value of the facilities. However, there have been recent transactions between independent parties to purchase plants at prices substantially below the carrying value of the facilities. Some of the facilities have been in bankruptcy and may not be representative of transactions outside of bankruptcy. Given these circumstances, should management be required to adjust the carrying value of the facilities

to fair value at some future point in time, the adjustment could be significant and could significantly impact the Company’s financial position and results of operation. No adjustment has been made in these financial statements for this uncertainty.

PACIFIC ETHANOL, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

The business and activities of the Company expose it to a variety of market risks, including risks related to changes in commodity prices and interest rates. The Company monitors and manages these financial exposures as an integral part of its risk management program. This program recognizes the unpredictability of financial

markets and seeks to reduce the potentially adverse effects that market volatility could have on operating results. The Company accounts for its use of derivatives related to its hedging activities pursuant to SFAS No. 133, under which the Company recognizes all of its derivative instruments in its statement of financial position as either assets or liabilities, depending on the rights or obligations under the contracts, unless the contracts qualify as a normal purchase or normal sale. Derivative instruments

are measured at fair value. Changes in the derivative’s fair value are recognized currently in income unless specific hedge accounting criteria are met. Special accounting for qualifying hedges allows a derivative’s effective gains and losses to be deferred in accumulated other comprehensive income and later recorded together with the gains and losses to offset related results on the hedged item in income. Companies must formally document, designate and assess the effectiveness of transactions that

receive hedge accounting.

Commodity Risk – Cash Flow Hedges – The Company uses derivative instruments

to protect cash flows from fluctuations caused by volatility in commodity prices in order to protect gross profit margins from potentially adverse effects of market and price volatility on ethanol sale and purchase commitments where the prices are set at a future date and/or if the contracts specify a floating or index-based price for ethanol. In addition, the Company hedges anticipated sales of ethanol to minimize its exposure to the potentially adverse effects of price volatility. These derivatives are designated

and documented as SFAS No. 133 cash flow hedges and effectiveness is evaluated by assessing the probability of the anticipated transactions and regressing commodity futures prices against the Company’s purchase and sales prices. Ineffectiveness, which is defined as the degree to which the derivative does not offset the underlying exposure, is recognized immediately in cost of goods sold.

For the three months ended June 30, 2009 and 2008, losses from effectiveness in the amount of $34,000 and $0, respectively, were recorded in cost of goods sold. For the six months ended June 30, 2009 and 2008, losses from effectiveness in the amount of $114,000 and gains of $5,277,000, respectively, were recorded in cost

of goods sold. For the three months ended June 30, 2009 and 2008, losses from ineffectiveness in the amount of $21,000 and $0, respectively, were recorded in cost of goods sold. For the six months ended June 30, 2009 and 2008, losses from ineffectiveness in the amount of $85,000 and $1,033,000, respectively, were recorded in cost of goods sold. There were no notional balances remaining on these derivatives as of June 30, 2009 and December 31, 2008.

Commodity Risk – Non-Designated Hedges – As part of the Company’s risk management strategy, it uses forward contracts on corn, crude oil and reformulated blendstock for oxygenate blending gasoline to lock in prices for

certain amounts of corn, denaturant and ethanol, respectively. These derivatives are not designated under SFAS No. 133 for special hedge accounting treatment. The changes in fair value of these contracts are recorded on the balance sheet and recognized immediately in cost of goods sold. For the three months ended June 30, 2009 and 2008, the Company recognized a gain of $139,000 and a loss of $918,000, respectively, and for the six months ended June 30, 2009 and 2008, the Company recognized a gain of $135,000

and a loss of $2,934,000, respectively, as the change in the fair value of these contracts. The notional balances remaining on these contracts as of June 30, 2009 and December 31, 2008 were $0 and $4,215,000, respectively.

PACIFIC ETHANOL, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

Interest Rate Risk – As part of the Company’s interest rate risk management strategy, the Company uses derivative instruments to minimize significant unanticipated income fluctuations that may arise from rising variable interest

rate costs associated with existing and anticipated borrowings. To meet these objectives the Company purchased interest rate caps and swaps. The rate for notional balances of interest rate caps ranging from $4,268,000 to $17,561,000 is 5.50%-6.00% per annum. The rate for notional balances of interest rate swaps ranging from $543,000 to $42,361,000 is 5.01%-8.16% per annum.

These derivatives are designated and documented as SFAS No. 133 cash flow hedges and effectiveness is evaluated by assessing the probability of anticipated interest expense and regressing the historical value of the rates against the historical value in the existing and anticipated debt. Ineffectiveness, reflecting the

degree to which the derivative does not offset the underlying exposure, is recognized immediately in other income (expense). For the three months ended June 30, 2009 and 2008, losses from effectiveness in the amount of $0 and $25,000, gains from ineffectiveness in the amount of $0 and $102,000 and gains of $834,000 and $897,000 from undesignated hedges, respectively, were recorded in other expense. For the six months ended June 30, 2009 and 2008, losses from effectiveness in the amount of $0 and $51,000, gains

from ineffectiveness in the amount of $0 and $182,000 and gains of $1,474,000 and losses of $4,149,000 from undesignated hedges, respectively, were recorded in other expense.

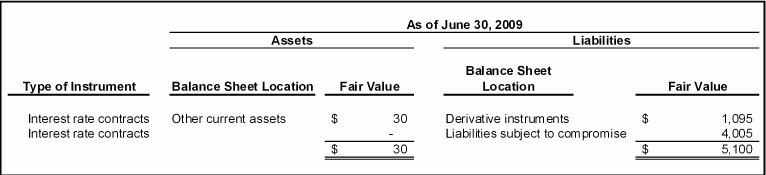

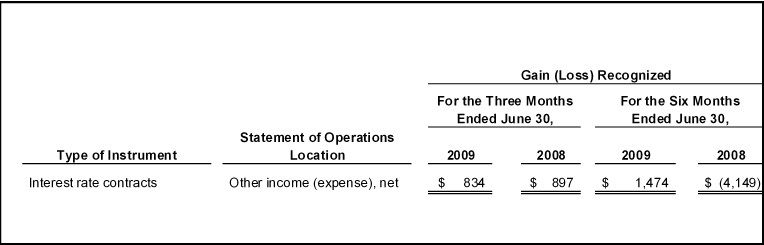

The classification and amounts of the Company’s derivatives not designated as hedging instruments are as follows (in thousands):

The classification and amounts of the Company’s recognized gains (losses) for its derivatives not designated as hedging instruments are as follow (in thousands):

The gains for the three months ended June 30, 2009 resulted primarily from the Company’s efforts to restructure its debt financing and, therefore, making it not probable that the related borrowings would be paid as designated. As such the Company de-designated certain of its interest rate caps and swaps. The losses

for the three months ended March 31, 2008 resulted primarily from the Company’s deferral of constructing its Imperial Valley facility.

PACIFIC ETHANOL, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

Long-term borrowings are summarized in the table below (in thousands):

| |

|

|

|

|

|

|

|

Notes payable to related party |

|

$ |

31,500 |

|

|

$ |

31,500 |

|

|

DIP Financing |

|

|

24,556 |

|

|

|

— |

|

|

Notes payable to related parties |

|

|

2,000 |

|

|

|

— |

|

|

Kinergy operating line of credit |

|

|

1,172 |

|

|

|

10,482 |

|

|

Swap note |

|

|

14,250 |

|

|

|

14,987 |

|

|

Variable rate note |

|

|

— |

|

|

|

582 |

|

|

Front Range operating line of credit |

|

|

1,200 |

|

|

|

1,200 |

|

|

Water rights capital lease obligations |

|

|

1,115 |

|

|

|

1,123 |

|

|

Term loans and working capital lines of credit |

|

|

— |

|

|

|

246,483 |

|

| |

|

|

75,793 |

|

|

|

306,357 |

|

|

Less short-term portion |

|

|

(62,255 |

) |

|

|

(291,925 |

) |

|

Long-term debt |

|

$ |

13,538 |

|

|

$ |

14,432 |

|

Notes Payable to Related Party – The Company has certain notes payable in favor of Lyles United, LLC and Lyles Mechanical Co. (collectively, “Lyles”) in the amounts of $30,000,000 and $1,500,000, which were due March

15, 2009 and March 31, 2009, respectively. In February 2009, the Company notified Lyles that it would not be able to pay these notes and entered into a forbearance agreement with Lyles. Under the terms of the forbearance agreement, Lyles agreed to forbear from exercising its rights and remedies against the Company through April 30, 2009. These forbearances have not been extended.

DIP Financing – Certain of the Bankrupt Debtors’ existing lenders (the “DIP Lenders”) entered into a credit agreement for up to a total of $20,000,000 (“DIP Financing”), not including the DIP Rollup

(as defined below) amount. The DIP Financing was approved by the Bankruptcy Court on June 3, 2009 and provides for a first priority lien in the Chapter 11 Filings. Proceeds of the DIP Financing will be used, among other things, to fund the working capital and general corporate needs of the Company and the costs of the Chapter 11 Filings in accordance with an approved budget. The DIP Financing matures in mid-November 2009, or sooner if certain covenants are not maintained. These covenants include various

reporting requirements to the DIP Lenders, as well as confirmation of a plan of reorganization prior to the maturity date. The Company believes it is in compliance with the DIP Financing covenants. The DIP Financing allows the DIP Lenders a first priority lien on a dollar-for-dollar basis of their term loans and working capital lines of credit funded prior to the Chapter 11 Filings for each dollar of DIP Financing. As the Bankrupt Debtors draw down on their DIP Financing, an equivalent amount is reclassified

from liabilities subject to compromise to DIP financing (“DIP Rollup”). As of June 30, 2009, the Bankrupt Debtors have received proceeds in the amount of $12,278,000 from the DIP Financing. After accounting for the DIP Rollup, the DIP Financing has a total balance of $24,556,000. The interest rate for the three months ended June 30, 2009, was approximately 14% per annum.

Notes Payable to Related Parties – On March 31, 2009, the Company’s Chairman of the Board and its Chief Executive Officer provided funds totaling $2,000,000 for general cash and operating purposes, in exchange for two unsecured

notes payable from the Company. Interest on the unpaid principal amount accrues at a rate per annum of 8.00%. All principal and accrued and unpaid interest on the notes is due and payable on March 31, 2010.

PACIFIC ETHANOL, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

Kinergy Operating Line of Credit – In February 2009, Kinergy determined it had violated certain of its covenants, including its EBITDA covenant for 2008 in its operating line of credit of up to $40,000,000 (“Line of Credit”),

and as a result, entered into an amendment and forbearance agreement (“Forbearance Agreement”) which was extended in March 2009 with its lender. The Forbearance Agreement identified certain defaults under the Line of Credit, as to which Kinergy’s lender agreed to forebear from exercising its rights and remedies under the Line of Credit commencing February 13, 2009 through April 30, 2009. The Forbearance Agreement reduced the aggregate amount of the credit facility from up to $40,000,000 to $10,000,000.

The Forbearance Agreement also increased the applicable interest rates. Kinergy may borrow under the Line of Credit based upon (i) a rate equal to (a) the London Interbank Offered Rate (“LIBOR”), divided by 0.90 (subject to change based upon the reserve percentage in effect from time to time under Regulation

D of the Board of Governors of the Federal Reserve System), plus (b) 4.50% depending on the amount of Kinergy’s EBITDA for a specified period, or (ii) a rate equal to (a) the greater of the prime rate published by Wachovia Bank from time to time, or the federal funds rate then in effect plus 0.50%, plus (b) 2.25% depending on the amount of Kinergy’s EBITDA for a specified period. Kinergy’s obligations under the Line of Credit are secured by a first-priority security interest in all of its assets

in favor of its lender.

On May 17, 2009, Kinergy and the Company entered into an Amendment and Waiver Agreement (“Amendment”) with Kinergy’s lender. Under the Amendment, Kinergy’s monthly unused line fee increased from 0.375% to 0.500% of the amount by which the maximum credit under the Line of Credit exceeds the average

daily principal balance. In addition, the Amendment imposed a new $5,000 monthly servicing fee. The Amendment also limited most payments that may be made by Kinergy to the Company as reimbursement for management and other services provided by the Company to Kinergy to $600,000 in any three month period and $2,400,000 in any twelve month period. The Amendment amends the definition of “Material Adverse Effect” to exclude the Chapter 11 Filings and certain other matters and clarifies that certain events

of default do not extend to the Bankrupt Debtors. However, the Amendment further made many events of default that previously were applicable only to Kinergy now applicable to the Company and its subsidiaries except for certain specified subsidiaries including the Bankrupt Debtors. Under the Amendment, the term of the Line of Credit was reduced from three years to a term expiring on October 31, 2010. The Amendment also removed the early termination fee that would be payable in the event Kinergy terminated the

Line of Credit prior to the conclusion of the term. In addition, the Amendment amended and restated Kinergy’s EBITDA covenants. The Amendment also prohibited Kinergy from incurring any additional indebtedness (other than certain intercompany indebtedness) or making any capital expenditures in excess of $100,000 absent the lender’s prior consent. Further, under the Amendment, the lender waived all existing defaults under the Line of Credit. Kinergy was required to pay an amendment fee of

$200,000 to the lender. Except as disclosed in the following paragraph, management believes that Kinergy was in compliance with its covenants as of June 30, 2009.

The Amendment also requires that, on or before May 31, 2009, the lender shall have received copies of financing agreements, in form and substance reasonably satisfactory to the lender, among the Company and certain of its subsidiaries and Lyles United, LLC, which agreements shall provide, among other things, for (i) a

credit facility available to the Company of up to $2,500,000 over a term of eighteen months (or such shorter term but in no event prior to the maturity date of the Loan Agreement), (ii) the grant by the Company to Lyles United, LLC of a security interest in substantially all of the Company’s assets, including a pledge by the Company to Lyles United, LLC of the equity interest of the Company in Kinergy, and (iii) the use by the Company of borrowings thereunder for general corporate and other purposes in

accordance with the terms thereof. As of June 30, 2009, the Company had not obtained the aforementioned financing with Lyles United, LLC. This has caused Kinergy to be out of compliance with this covenant. Kinergy’s lender, however, has continued to fund the Line of Credit under the terms described above, with no further amendments.

PACIFIC ETHANOL, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

Swap Note – Front Range is subject to certain loan covenants under the terms of its Swap Note. Under these covenants, Front Range is required to maintain, on a quarterly basis, a certain fixed-charge coverage ratio, a minimum level

of working capital and a minimum level of net worth. The covenants also set a maximum amount of additional debt that may be incurred by Front Range. The covenants also limit annual distributions that may be made to owners of Front Range, including the Company, based on Front Range’s leverage ratio. As of December 31, 2008 and March 31, 2009, Front Range was out of compliance with certain of its covenants and has since obtained a waiver from its lender. Under the terms of the waiver, the lender changed the

covenant to an annual calculation from a quarterly calculation. Further, the available long term revolving note was reduced from $5,000,000 to $2,500,000, with an August 10, 2011 maturity date. The interest rate was adjusted to the greater of 5% or the 30 day LIBOR rate plus 3.25%-4.00% depending on Front Range’s debt-to-net worth ratio. As of June 30, 2009, the Company believes it is in compliance with its revised covenants with its lender.

Term Loans & Working Capital Lines of Credit – In connection with financing the Company’s construction of its four ethanol production facilities, in 2007, the Company entered into a debt financing transaction through its

wholly-owned indirect subsidiaries. These subsidiaries are now the Bankrupt Debtors and these loans are discussed in more detail in Note 9.

|

9. |

LIABILITIES SUBJECT TO COMPROMISE. |

Liabilities subject to compromise refers to prepetition obligations which may be impacted by the Chapter 11 Filings. These amounts represent the Company’s current estimate of known or potential prepetition obligations to be resolved in connection with the Chapter 11 Filings.

Differences between liabilities estimated and the claims filed, or to be filed, will be investigated and resolved in connection with the claims resolution process. The Company will continue to evaluate these liabilities during the Chapter 11 Filings and adjust amounts as necessary.

Liabilities subject to compromise are as follows (in thousands):

| |

|

|

|

|

Term loans |

|

$ |

216,435 |

|

|

Working capital lines of credit |

|

|

17,770 |

|

|

Accrued interest payable |

|

|

10,951 |

|

|

Derivative instruments – interest rate swaps |

|

|

4,005 |

|

|

Accounts payable trade and accrued expenses |

|

|

3,718 |

|

|

Total liabilities subject to compromise |

|

$ |

252,879 |

|

Term Loans & Working Capital Lines of Credit – In connection with financing the Company’s construction of its four ethanol production facilities, in 2007, the Company entered into a debt financing transaction (the “Debt

Financing”) in the aggregate amount of up to $250,769,000 through its wholly-owned indirect subsidiaries. These subsidiaries are now the Bankrupt Debtors. The Debt Financing included four term loans and four working capital lines of credit. In addition, the subsidiaries utilized approximately $825,000 of the working capital and letter of credit facility to obtain a letter of credit, which was also outstanding at June 30, 2009 and December 31, 2008. The obligations under the Debt Financing are secured by

a first-priority security interest in all of the equity interests in the subsidiaries and substantially all their assets. The Chapter 11 Filings constituted an event of default under the Debt Financing. Under the terms of the Debt Financing, upon the Chapter 11 Filings, the outstanding principal amount of, and accrued interest on, the amounts owed in respect of the Debt Financing became immediately due and payable.

PACIFIC ETHANOL, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

As discussed above in Note 8, the DIP Lenders provided DIP Financing for up to a total of $20,000,000. The DIP Financing was approved by the Bankruptcy Court on June 3, 2009 and provides for a first priority lien in the Chapter 11 Filings. The DIP Financing also allows the DIP Lenders a first priority lien on a dollar-for-dollar

basis of their term loans and working capital lines of credit funded prior to the Chapter 11 Filings for each dollar of DIP Financing. As the Bankrupt Debtors draw down on their DIP Financing, an equivalent amount is reclassified from liabilities subject to compromise to DIP Financing. As of June 30, 2009, the Bankrupt Debtors have received funds in the amount of $12,278,000 from the DIP Financing,

therefore reducing an equal amount owed under the Debt Financing that has been reclassified and reported as DIP Financing.

|

10. |

COMMITMENTS AND CONTINGENCIES. |

Purchase Commitments – At June 30, 2009, the Company had purchase contracts with its suppliers to purchase certain quantities of ethanol, corn and denaturant. These fixed- and indexed-price commitments will be delivered throughout

the remainder of 2009. Outstanding balances on fixed-price contracts for the purchases of materials are indicated below and volumes indicated in the indexed-price portion of the table are additional purchase commitments at publicly-indexed sales prices determined by market prices in effect on their respective transaction dates (in thousands):

| |

|

Fixed-Price Contracts |

|

|

Ethanol |

|

$ |

4,781 |

|

|

Corn |

|

|

2,792 |

|

|

Denaturant |

|

|

446 |

|

|

Total |

|

$ |

8,019 |

|

| |

|

Indexed-Price Contracts

(Volume) |

|

|

Ethanol (gallons) |

|

|

19,277 |

|

|

Corn (bushels) |

|

|

10,973 |

|

Sales Commitments – At June 30, 2009, the Company had entered into sales contracts with its major customers to sell certain quantities of ethanol, WDG, and syrup. The volumes indicated in the indexed price contracts table will be

sold at publicly-indexed sales prices determined by market prices in effect on their respective transaction dates (in thousands):

| |

|

Fixed-Price Contracts |

|

|

Ethanol |

|

$ |

1,801 |

|

|

WDG |

|

|

6,524 |

|

|

Syrup |

|

|

2,399 |

|

|

Total |

|

$ |

10,724 |

|

| |

|

Indexed-Price Contracts

(Volume) |

|

|

Ethanol (gallons) |

|

|

20,878 |

|

Litigation – General – The Company is subject to legal proceedings, claims and litigation arising in the ordinary course of business. While the amounts claimed may be

substantial, the ultimate liability cannot presently be determined because of considerable uncertainties that exist. Therefore, it is possible that the outcome of those legal proceedings, claims and litigation could adversely affect the Company’s quarterly or annual operating results or cash flows when resolved in a future period. However, based on facts currently available, management believes that such matters will not adversely affect the Company’s financial position, results of operations or cash

flows.

Litigation – Western Ethanol Company – On January 9, 2009, Western Ethanol Company, LLC (“Western Ethanol”) filed a complaint in the Superior Court of the State of California (the “Superior Court”)

naming Kinergy as defendant. In the complaint, Western Ethanol alleges that Kinergy breached an alleged agreement to buy and accept delivery of a fixed amount of ethanol. On January 12, 2009, Western Ethanol filed an application for issuance of right to attach order and order for issuance of writ of attachment. On February 10, 2009, the Superior Court granted the right to attach order and order for issuance of writ of attachment against Kinergy in the amount of approximately $3,700,000. On February 11, 2009,

Kinergy filed an answer to the complaint. On May 14, 2009, Kinergy entered into an Agreement with Western Ethanol under which Western Ethanol agreed to terminate all notices, writs of attachment issued to the Sheriff of any county other than Contra Costa County, and all notices of levy, liens, and similar claims or actions except as to a levy against a specified Kinergy receivable in the amount of $1,350,000. Kinergy agreed to have the $1,350,000 receivable paid over to the Contra Costa County Sheriff in compliance

with and in satisfaction of the levy on the receivable to be held pending final outcome of the litigation. The Company has recorded this receivable in other current assets on its consolidated balance sheet. The Agreement does not otherwise alter the parties’ respective positions on the merits of the case and Kinergy intends to continue to vigorously defend against Western Ethanol’s claims.

Litigation – Barry Spiegel – On December 22, 2005, Barry J. Spiegel, a former shareholder and director of Accessity, filed a complaint in the Circuit Court of the 17th Judicial District in and for Broward County, Florida (Case

No. 05018512) (the “State Court Action”) against Barry Siegel, Philip Kart, Kenneth Friedman and Bruce Udell (collectively, the “Individual Defendants”). Messrs. Udell and Friedman are former directors of Accessity and Pacific Ethanol. Mr. Kart is a former executive officer of Accessity and Pacific Ethanol. Mr. Siegel was a former director and executive officer of Accessity and Pacific Ethanol.

The State Court Action relates to the Share Exchange Transaction and purports to state the following five counts against the Individual Defendants: (i) breach of fiduciary duty, (ii) violation of the Florida Deceptive and Unfair Trade Practices Act, (iii) conspiracy to defraud, (iv) fraud, and (v) violation of Florida’s

Securities and Investor Protection Act. Mr. Spiegel based his claims on allegations that the actions of the Individual Defendants in approving the Share Exchange Transaction caused the value of his Accessity common stock to diminish and is seeking approximately $22.0 million in damages. On March 8, 2006, the Individual Defendants filed a motion to dismiss the State Court Action. Mr. Spiegel filed his response in opposition on May 30, 2006. The Court granted the motion to dismiss by Order dated December 1, 2006,

on the grounds that, among other things, Mr. Spiegel failed to bring his claims as a derivative action.

PACIFIC ETHANOL, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

On February 9, 2007, Mr. Spiegel filed an amended complaint which purports to state the following five counts: (i) breach of fiduciary duty, (ii) fraudulent inducement, (iii) violation of Florida’s Securities and Investor Protection Act, (iv) fraudulent concealment, and (v) breach of fiduciary duty of disclosure.

The amended complaint included Pacific Ethanol as a defendant. On March 30, 2007, Pacific Ethanol filed a motion to dismiss the amended complaint. Before the Court could decide that motion, on June 4, 2007, Mr. Spiegel amended his complaint, which purports to state two counts: (i) breach of fiduciary duty and (ii) fraudulent inducement. The first count is alleged against the Individual Defendants and the second count is alleged against the Individual Defendants and Pacific Ethanol. The amended complaint was,

however, voluntarily dismissed on August 27, 2007, by Mr. Spiegel as to Pacific Ethanol. In March 2009, Mr. Spiegel sought and obtained leave to file another amended complaint which renewed his case against Pacific Ethanol, and the amended pleading named three additional individual defendants, and asserted the following three counts: (i) breach of fiduciary duty, (ii) fraudulent inducement, and (iii) aiding and abetting breach of fiduciary duty. The first two counts are alleged against the Individual Defendants.

With respect to the third count, the pleading alleges claims a claim against Pacific Ethanol California, Inc. (formerly known as Pacific Ethanol, Inc.), as well as against individual William Jones, Neil Koehler and Ryan Turner. Messrs. Jones, Koehler and Turner are current and former officers and directors of Pacific Ethanol. A response to the recent amended pleading is due to be filed on August 14, 2009.

Litigation – Delta-T Corporation – On August 18, 2008, Delta-T Corporation filed suit in the United States District Court for the Eastern District of Virginia (the “Virginia Federal Court case”), naming Pacific

Ethanol, Inc. as a defendant, along with its subsidiaries Pacific Ethanol Stockton, LLC, Pacific Ethanol Imperial, LLC, Pacific Ethanol Columbia, LLC, Pacific Ethanol Magic Valley, LLC and Pacific Ethanol Madera, LLC. The suit alleges breaches of the parties’ Engineering, Procurement and Technology License Agreements, breaches of a subsequent term sheet and letter agreement and breaches of indemnity obligations. The complaint seeks specified contract damages of approximately $6.5 million, along with other

unspecified damages. All of the defendants moved to dismiss the Virginia Federal Court case for lack of personal jurisdiction and on the ground that all disputes between the parties must be resolved through binding arbitration, and, in the alternative, moving to stay the Virginia Federal Court Case pending arbitration. In January 2009, these motions were granted by the Court, compelling the case to arbitration with the American Arbitration Association (“AAA”). By letter dated June 10, 2009, the AAA

notified the parties to the arbitration that the matter was automatically stayed as a result of the Chapter 11 Filings. Delta-T Corporation subsequently sought to continue the arbitration as to Pacific Ethanol, Inc.

On March 18, 2009 Delta-T Corporation filed a cross-complaint against Pacific Ethanol, Inc. and Pacific Ethanol Imperial, LLC in the Superior Court of the State of California in and for the County of Imperial. The cross-complaint arises out of a suit by OneSource Distributors, LLC against Delta-T Corporation. On March

31, 2009, Delta-T Corporation and Bateman Litwin N.V, a foreign corporation, filed a third-party complaint in the United States District Court for the District of Minnesota naming Pacific Ethanol, Inc. and Pacific Ethanol Imperial, LLC as defendants. The third-party complaint arises out of a suit by Campbell-Sevey, Inc. against Delta-T Corporation. On April 6, 2009 Delta-T Corporation filed a cross-complaint against Pacific Ethanol, Inc. and Pacific Ethanol Imperial, LLC in the Superior Court of the State of

California in and for the County of Imperial. The cross-complaint arises out of a suit by GEA Westfalia Separator, Inc. against Delta-T Corporation. Each of these actions allegedly relate to the aforementioned Engineering, Procurement and Technology License Agreements and Delta-T Corporation’s performance of services thereunder. The third-party suit and the cross-complaints assert many of the factual allegations in the Virginia Federal Court case and seek unspecified damages.

In connection with the Chapter 11 Filings, the Bankrupt Debtors moved the United States Bankruptcy Court for the District of Delaware to enter a preliminary injunction staying and enjoining all of the aforementioned litigation and arbitration proceedings with Delta-T Corporation. On August 6, 2009, the Delaware court