| x |

ANNUAL

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE

ACT OF

1934 For the fiscal year ended December 31,

2006

|

| ¨ |

TRANSITION

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE

ACT OF

1934 For the transition period from

to

|

|

Delaware

|

41-2170618

|

|

(State

or other jurisdiction of incorporation or

organization)

|

(I.R.S.

Employer Identification

No.)

|

|

400

Capitol Mall, Suite 2060, Sacramento, California

|

95814

|

|

(Address

of principal executive offices)

|

(Zip

Code)

|

|

Large

accelerated filer x

|

Accelerated

filer ¨

|

Non-accelerated

filer ¨

|

|

Page

|

||

|

PART I

|

||

|

Item

1.

|

Business

|

1

|

|

Item

1A.

|

Risk

Factors.

|

13

|

|

Item

1B.

|

Unresolved

Staff Comments.

|

24

|

|

Item

2.

|

Properties.

|

24

|

|

Item

3.

|

Legal

Proceedings.

|

24

|

|

Item

4.

|

Submission

of Matters to a Vote of Security Holders.

|

26

|

|

|

PART

II

|

|

|

Item

5.

|

Market

For Registrant’s Common Equity, Related Stockholder Matters and Issuer

Purchases of Equity Securities.

|

27

|

|

Item

6.

|

Selected

Financial Data.

|

30

|

|

Item

7.

|

Management’s

Discussion and Analysis of Financial Condition and Results of

Operations.

|

31

|

|

Item

7A.

|

Quantitative

and Qualitative Disclosures About Market Risk.

|

49

|

|

Item

8.

|

Financial

Statements and Supplementary Data.

|

51

|

|

Item

9.

|

Changes

in and Disagreements with Accountants on Accounting and Financial

Disclosure.

|

51

|

|

Item

9A.

|

Controls

and Procedures

|

51

|

|

Item

9B.

|

Other

Information.

|

59

|

|

|

PART

III

|

|

|

Item

10.

|

Directors,

Executive Officers and Corporate Governance

|

60

|

|

Item

11.

|

Executive

Compensation

|

60

|

|

Item

12.

|

Security

Ownership of Certain Beneficial Owners and Management and Related

Stockholder Matters

|

60

|

|

Item

13.

|

Certain

Relationships and Related Transactions, and Director

Independence

|

60

|

|

Item

14.

|

Principal

Accounting Fees and Services

|

60

|

|

|

PART

IV

|

|

|

Item

15.

|

Exhibits,

Financial Statement Schedules

|

60

|

|

Index

to Financial Statements

|

F-1

|

|

|

Index

to Exhibits

|

||

|

Signatures

|

||

|

Exhibits

Filed With This Report

|

|

|

|

o

|

Locations

near fuel blending facilities will enable lower ethanol transportation

costs and enjoy timing and logistical advantages over competing locations

requiring ethanol to be shipped over much longer distances.

|

|

o

|

Locations

adjacent to major rail lines will enable the purchase of corn from

major

corn-producing regions for efficient delivery in large-scale trains.

|

|

o

|

Locations

near large concentrations of dairy and/or beef cattle will enable

delivery

of WDG over short distances without the need for costly drying processes.

|

|

Madera

Facility

|

Front

Range

Facility(1)

|

Boardman

Facility(2)

|

California

Facility(2)

|

Imperial

Valley

Facility(2)

|

Magic

Valley

Facility(2)

|

|

|

Location

|

Madera,

CA

|

Windsor,

CO

|

Boardman,

OR

|

TBA

|

Brawley,

CA

|

Burley,

ID

|

|

Quarter/Year

completed or scheduled to be completed

|

4th

Qtr., 2006

|

2nd

Qtr., 2006

|

2nd

Qtr., 2007

|

2nd

Qtr., 2008

|

2nd

Qtr., 2008

|

2nd

Qtr., 2008

|

|

Annual

ethanol nameplate production capacity (in millions of

gallons)

|

35

|

40

|

35

|

50

|

50

|

50

|

|

Ownership

|

100%

|

42%

|

100%

|

100%

|

100%

|

100%

|

|

Primary

energy source

|

Natural

Gas

|

Natural

Gas

|

Natural

Gas

|

Natural

Gas

|

Natural

Gas

|

Natural

Gas

|

|

Estimated

annual WDG production capacity (in thousands of tons)

|

293

|

335

|

293

|

418

|

418

|

418

|

|

·

|

restrictions

on our existing and proposed business operations and/or the need

to

install enhanced or additional controls;

|

|

|

·

|

the

need to obtain and comply with permits and

authorizations;

|

|

|

·

|

liability

for exceeding applicable permit limits or legal requirements, in

certain

cases for the remediation of contaminated soil and groundwater

at our

facilities, contiguous and adjacent properties and other properties

owned

and/or operated by third parties; and

|

|

|

·

|

specifications

for the ethanol we market and

produce.

|

|

·

|

changing

conditions in the ethanol and fuel markets as well as other commodity

markets such as corn;

|

|

|

·

|

the

volume and timing of the receipt of orders for ethanol from major

customers;

|

|

|

·

|

competitive

pricing pressures;

|

|

|

·

|

our

ability to produce, sell and deliver ethanol on a cost-effective

and

timely basis;

|

|

|

·

|

the

introduction and announcement of one or more new alternatives to

ethanol

by our competitors;

|

|

|

·

|

changes

in market valuations of similar companies;

|

|

|

·

|

stock

market price and volume fluctuations generally;

|

|

|

·

|

regulatory

developments or increased enforcement;

|

|

|

·

|

fluctuations

in our quarterly or annual operating results;

|

|

|

·

|

additions

or departures of key personnel;

|

|

|

·

|

our

inability to obtain construction, acquisition, capital equipment

and/or

working capital financing; and

|

|

|

·

|

future

sales of our common stock or other

securities.

|

|

Price

Range

|

||

|

High

|

Low

|

|

|

Year

Ended December 31, 2005:

|

||

|

First

Quarter (January 1 - March 31)

|

$10.25

|

$5.49

|

|

Second

Quarter (April 1 - June 30)

|

12.94

|

8.58

|

|

Third

Quarter (July 1 - September 30)

|

11.20

|

7.78

|

|

Fourth

Quarter (October 1 - December 31)

|

13.48

|

7.71

|

|

Year

Ended December 31, 2006:

|

||

|

First

Quarter

|

$22.34

|

$9.99

|

|

Second

Quarter

|

42.39

|

20.14

|

|

Third

Quarter

|

25.45

|

13.76

|

|

Fourth

Quarter

|

19.08

|

12.58

|

|

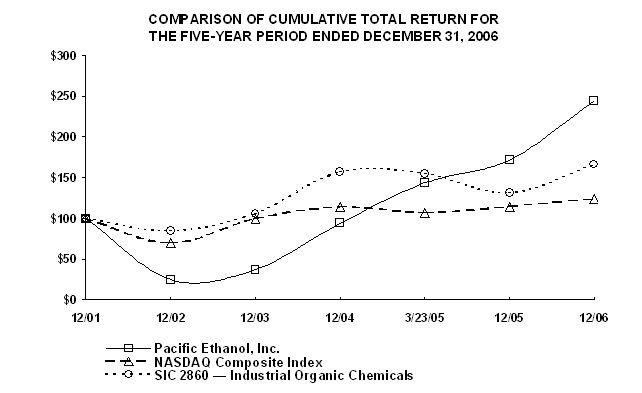

Cumulative

Total Return ($)

|

|||||||

|

12/01

|

12/02

|

12/03

|

12/04

|

3/23/05

|

12/05

|

12/06

|

|

|

PACIFIC

ETHANOL, INC.

|

100.00

|

24.60

|

37.30

|

94.13

|

143.65

|

171.75

|

244.29

|

|

THE

NASDAQ STOCK MARKET (U.S.) INDEX

|

100.00

|

69.66

|

99.71

|

113.79

|

106.87

|

114.47

|

124.20

|

|

SIC

2860—INDUSTRIAL ORGANIC CHEMICALS

|

100.00

|

84.41

|

105.89

|

156.97

|

154.98

|

130.92

|

166.23

|

|

Year

Ended December 31,

|

|||||||||||||

|

2006

|

2005

|

2004

|

2003

|

||||||||||

|

(in

thousands, except per share data)

|

|||||||||||||

|

Consolidated

Statements of Operations Data:

|

|

|

|

||||||||||

|

Net

sales

|

$

|

226,356

|

$

|

87,599

|

$

|

20

|

$

|

1,017

|

|||||

|

Cost

of goods sold

|

201,527

|

84,444

|

13

|

946

|

|||||||||

|

Gross

profit

|

24,829

|

3,155

|

7

|

71

|

|||||||||

|

Selling,

general and administrative expenses

|

24,641

|

12,638

|

2,277

|

648

|

|||||||||

|

Income

(loss) from operations

|

188

|

(9,483

|

)

|

(2,270

|

)

|

(577

|

)

|

||||||

|

Other

income (expense), net

|

3,426

|

(440

|

)

|

(532

|

)

|

(282

|

)

|

||||||

|

Non-controlling

interest in variable interest entity

|

(3,756

|

)

|

—

|

—

|

—

|

||||||||

|

Loss

from operations before income taxes

|

(142

|

)

|

(9,923

|

)

|

(2,802

|

)

|

(859

|

)

|

|||||

|

Provision

for income taxes

|

—

|

—

|

—

|

—

|

|||||||||

|

Net

loss

|

$

|

(142

|

)

|

$

|

(9,923

|

)

|

$

|

(2,802

|

)

|

$

|

(859

|

)

|

|

|

Preferred

stock dividends

|

$

|

(2,998

|

)

|

$

|

—

|

$

|

—

|

$

|

—

|

||||

|

Deemed

dividend on preferred stock

|

(84,000

|

)

|

—

|

—

|

—

|

||||||||

|

Loss

available to common stockholders

|

$

|

(87,140

|

)

|

$

|

(9,923

|

)

|

$

|

(2,802

|

)

|

$

|

(859

|

)

|

|

|

Loss

per common share, basic and diluted

|

$

|

(2.50

|

)

|

$

|

(0.40

|

)

|

$

|

(0.23

|

)

|

$

|

(0.07

|

)

|

|

|

Weighted-average

shares outstanding, basic and diluted

|

34,855

|

25,066

|

12,397

|

11,733

|

|||||||||

|

Consolidated

Balance Sheet Data:

|

|||||||||||||

|

Cash

and cash equivalents

|

$

|

44,053

|

$

|

4,521

|

$

|

—

|

$

|

249

|

|||||

|

Working

capital (deficit)

|

96,451

|

(2,894

|

)

|

(1,025

|

)

|

(358

|

)

|

||||||

|

Total

assets

|

453,820

|

48,185

|

7,179

|

6,560

|

|||||||||

|

Long-term

debt

|

28,970

|

1,995

|

4,013

|

—

|

|||||||||

|

Stockholders’

equity

|

298,445

|

28,516

|

1,356

|

1,368

|

|||||||||

|

·

|

fluctuations

in the market price of ethanol and its co-products;

|

|

·

|

the

projected growth or contraction in the ethanol and co-product market

in

which we operate;

|

|

·

|

our

strategies for expanding, maintaining or contracting our presence

in these

markets;

|

|

·

|

our

ability to successfully develop, finance, construct and operate our

planned ethanol production facilities;

|

|

·

|

anticipated

trends in our financial condition and results of operations;

and

|

|

·

|

our

ability to distinguish ourselves from our current and future competitors.

|

|

·

|

Net

sales. Our

increase in net sales in 2006 as compared to 2005 was primarily due

to the

following combination of factors:

|

|

o

|

Higher

sales volumes.

Total volume of ethanol sold as a principal and an agent increased

by 49.4

million gallons, or 94.5%, to 101.7 million gallons for 2006 from

52.3

million gallons for 2005. The substantial increase in sales volume

is

primarily due to additional supply provided under our ethanol marketing

agreements and the commencement of ethanol production.

|

|

o

|

Commencement

of ethanol production.

In the fourth quarter of 2006, we commenced producing ethanol and

its

co-products at our Madera facility and, based on our ownership interest

in

Front Range, began recording a proportionate amount of its net sales.

The

production and sale of ethanol and its co-products at our Madera

facility

and through Front Range contributed an aggregate of $25.9 million

in sales

for 2006.

|

|

o

|

Higher

ethanol prices.

Our average sales price of ethanol increased by $0.61 per gallon,

or

36.5%, to $2.28 per gallon for all gallons sold as a principal and

an

agent for 2006 as compared to $1.67 per gallon for 2005.

|

|

o

|

Partial

period comparison.

Our results of operations for 2006, including our net sales, include

our

operations and those of all of our wholly-owned subsidiaries, including

Kinergy Marketing, LLC, or Kinergy, for that entire period. However,

our

results of operations for 2005, including our net sales, exclude

Kinergy’s

net sales for the period from January 1, 2005 through March 22, 2005

in

the amount of $23.6 million. See “Share Exchange Transaction”

below.

|

|

·

|

Gross

profit. Our

gross profit margin increased to 10.9% for 2006 as compared to a

gross

profit margin of 3.6% for 2005. This increase was primarily due to

locking

in favorable margins through purchase and sale commitments consistent

with

our risk management guidelines at various times during 2006. The

increase

in our gross profit margins was also due to sales resulting from

ethanol

production, which typically generates higher gross profits than ethanol

marketing arrangements, at our Madera facility and also through Front

Range.

|

| · |

Selling,

general and administrative expenses.

Our selling, general and administrative expenses increased by $12.0

million to $24.6 million in 2006 as compared to $12.6 million in

2005;

however, these expenses decreased as a percentage of our net sales

due to

our substantial growth in net sales. Our selling, general and

administrative expenses decreased to 10.9% of net sales in 2006 as

compared to 14.4% of net sales in 2005.

|

|

·

|

the

market price of ethanol, which we believe will be impacted by the

degree

of competition in the ethanol market, the price of gasoline and related

petroleum products, and government regulation, including tax incentives;

|

|

·

|

the

market price of key production input commodities, including corn

and

natural gas;

|

|

·

|

our

ability to anticipate trends in the market price of ethanol, WDG,

and key

input commodities and implement appropriate risk management and

opportunistic strategies; and

|

|

·

|

the

proportion of our sales of ethanol produced at our facilities to

our sales

of ethanol produced by third-parties.

|

|

·

|

As

a merchant.

Sales as a merchant consist of sales to customers through purchases

from

third-party suppliers in which we may or may not obtain physical

control

of the ethanol or co-products, though ultimately titled to us, in

which

shipments are directed from our suppliers to our terminals or direct

to

our customers but for which we accept the risk of loss in the

transactions.

|

|

·

|

As

a producer.

Sales as a producer consist of sales of our inventory produced at

our

facilities, including by Front

Range.

|

|

·

|

As

an agent.

Sales as an agent consist of sales to customers through purchases

from

third-party suppliers in which, depending upon the terms of the

transactions, title to the product may technically pass to us, but

risk of

loss in the transactions does not since all transacted sales prices

flow

back to our third-party suppliers. When acting as an agent for third-party

suppliers, we conduct back-to-back purchases and sales in which we

match

ethanol purchase and sales contracts of like quantities and delivery

periods. We receive a predetermined service fee under these transactions

and therefore act predominantly in an agency

capacity.

|

|

Cash

and cash equivalents

|

$

|

742

|

||

|

Investments

|

7,058

|

|||

|

Accounts

receivable

|

3,520

|

|||

|

Inventories

|

3,535

|

|||

|

Other

current assets

|

235

|

|||

|

Property

and equipment

|

92,376

|

|||

|

Other

long-term assets

|

584

|

|||

|

Intangibles

- customer backlog

|

3,900

|

|||

|

Intangibles

- non-compete covenants

|

400

|

|||

|

Goodwill

|

80,607

|

|||

|

Current

portion of long-term debt

|

(3,395

|

)

|

||

|

Accounts

payable and accrued expenses

|

(4,591

|

)

|

||

|

Long-term

debt

|

(28,753

|

)

|

||

|

Non-controlling

interest in variable interest entity

|

(90,606

|

)

|

||

|

Net

Assets

|

$

|

65,612

|

|

2006

|

2005

|

||||||

|

Commodity

futures

|

$

|

646

|

$

|

—

|

|||

|

Commodity

options

|

(24

|

)

|

—

|

||||

|

Interest

rate options

|

(17

|

)

|

—

|

||||

|

Total

|

$

|

605

|

$

|

—

|

|||

|

·

|

The

first two data columns in the tables show the absolute results for

each

period presented.

|

|

·

|

The

columns entitled “Dollar Variance” and “Percentage Variance” show the

change in results, both in dollars and percentages. These two columns

show

favorable changes as a positive and unfavorable changes as negative.

For

example, when our net sales increase from one period to the next,

that

change is shown as a positive number in both columns. Conversely,

when

expenses increase from one period to the next, that change is shown

as a

negative in both columns.

|

|

·

|

The

last two columns in the tables show the results for each period as

a

percentage of net sales.

|

|

|

|

|

Year

Ended

|

Dollar

Variance

|

Percentage

Variance

|

Results

as a Percentage

of

Net Sales for the

Year

Ended

|

|||||||||||||

|

December

31,

|

Favorable

|

Favorable

|

December

31,

|

||||||||||||||||

|

2006

|

2005

|

(Unfavorable)

|

(Unfavorable)

|

2006

|

2005

|

||||||||||||||

|

(in

thousands)

|

|||||||||||||||||||

|

Net

sales

|

$

|

226,356

|

$

|

87,599

|

$

|

138,757

|

158.4

|

%

|

100.0

|

%

|

100.0

|

%

|

|||||||

|

Cost

of sales

|

201,527

|

84,444

|

(117,083

|

)

|

(138.6

|

)

|

89.0

|

96.4

|

|||||||||||

|

Gross

profit

|

24,829

|

3,155

|

21,674

|

687.0

|

10.9

|

3.6

|

|||||||||||||

|

Selling,

general and administrative expenses

|

24,641

|

12,638

|

(12,003

|

)

|

(94.9

|

)

|

10.9

|

14.4

|

|||||||||||

|

Income

(loss) from operations

|

188

|

(9,483

|

)

|

9,671

|

101.9

|

0.1

|

(10.8

|

)

|

|||||||||||

|

Other

income (expense), net

|

3,426

|

(440

|

)

|

3,866

|

878.6

|

1.5

|

(0.5

|

)

|

|||||||||||

|

Income

(loss) before non-controlling interest in variable interest

entity

|

3,614

|

(9,923

|

)

|

13,537

|

136.4

|

1.6

|

(11.3

|

)

|

|||||||||||

|

Provision

for income taxes

|

—

|

—

|

—

|

—

|

—

|

—

|

|||||||||||||

|

Non-controlling

interest in variable interest entity

|

(3,756

|

)

|

—

|

(3,756

|

)

|

(100.0

|

)

|

(1.7

|

)

|

—

|

|||||||||

|

Net

loss

|

$

|

(142

|

)

|

$

|

(9,923

|

)

|

$

|

9,781

|

98.6

|

%

|

(0.1

|

)%

|

(11.3

|

)%

|

|||||

|

Preferred

stock dividends

|

(2,998

|

)

|

—

|

(2,998

|

)

|

(100.0

|

)

|

(1.3

|

)

|

—

|

|||||||||

|

Deemed

dividend on preferred stock

|

(84,000

|

)

|

—

|

(84,000

|

)

|

(100.0

|

)

|

(37.1

|

)

|

—

|

|||||||||

|

Loss

available to common stockholders

|

$

|

(87,140

|

)

|

$

|

(9,923

|

)

|

$

|

(77,217

|

)

|

(778.2

|

)%

|

(38.5

|

)%

|

(11.3

|

)%

|

||||

|

Year

Ended

|

Dollar

Variance

|

Percentage

Variance

|

Results

as a Percentage

of

Net Sales for the

Year

Ended

|

||||||||||||||||

|

December

31,

|

Favorable

|

Favorable

|

December

31,

|

||||||||||||||||

|

2005

|

2004

|

(Unfavorable)

|

(Unfavorable)

|

2005

|

2004

|

||||||||||||||

|

(in

thousands)

|

|||||||||||||||||||

|

Net

sales

|

$

|

87,599

|

$

|

20

|

$

|

87,579

|

437,895.0

|

%

|

100.0

|

%

|

100.0

|

%

|

|||||||

|

Cost

of sales

|

84,444

|

13

|

(84,431

|

)

|

(649,469.2

|

)

|

96.4

|

65.0

|

|||||||||||

|

Gross

profit

|

3,155

|

7

|

3,148

|

44,971.4

|

3.6

|

35.0

|

|||||||||||||

|

Selling,

general and administrative expenses

|

10,995

|

2,277

|

(8,718

|

)

|

(382.8

|

)

|

12.6

|

11,385.0

|

|||||||||||

|

Feasibility

study expensed in connection with acquisition of ReEnergy

|

852

|

—

|

(852

|

)

|

(100.0

|

)

|

1.0

|

—

|

|||||||||||

|

Acquisition

cost expense in excess of cash received

|

481

|

—

|

(481

|

)

|

(100.0

|

)

|

0.5

|

—

|

|||||||||||

|

Discontinued

design of cogeneration facility

|

310

|

—

|

(310

|

)

|

(100.0

|

)

|

0.4

|

—

|

|||||||||||

|

Loss

from operations

|

(9,483

|

)

|

(2,270

|

)

|

(7,213

|

)

|

(317.8

|

)

|

(10.8

|

)

|

(11,350.0

|

)

|

|||||||

|

Total

other expense

|

(440

|

)

|

(532

|

)

|

92

|

17.3

|

(0.5

|

)

|

(2,660.0

|

)

|

|||||||||

|

Loss

from operations before income taxes

|

(9,923

|

)

|

(2,802

|

)

|

(7,121

|

)

|

(254.1

|

)

|

(11.3

|

)

|

(14,010.0

|

)

|

|||||||

|

Provision

for income taxes

|

—

|

—

|

—

|

—

|

—

|

—

|

|||||||||||||

|

Net

loss

|

$

|

(9,923

|

)

|

$

|

(2,802

|

)

|

$

|

(7,121

|

)

|

(254.1

|

)

|

(11.3

|

)%

|

(14,010.0

|

)%

|

||||

|

Contractual

Obligations

At

December 31, 2006

|

2007

|

2008

|

2009

|

2010

|

2011

|

Thereafter

|

Total

|

|||||||||||||||

|

Sourcing

commitments(1)

|

$

|

81,945

|

$

|

—

|

$

|

—

|

$

|

—

|

$

|

—

|

$

|

—

|

$

|

81,945

|

||||||||

|

Debt

principal(2)

|

4,030

|

2,910

|

3,158

|

3,425

|

18,359

|

—

|

31,882

|

|||||||||||||||

|

Debt

interest(2)

|

2,831

|

2,597

|

2,344

|

2,070

|

1,773

|

—

|

11,615

|

|||||||||||||||

|

Water

rights - capital lease, including interest(3)

|

160

|

160

|

160

|

160

|

160

|

800

|

1,600

|

|||||||||||||||

|

Operating

leases(4)

|

267

|

203

|

172

|

172

|

110

|

—

|

924

|

|||||||||||||||

|

Firm

capital commitments(5)

|

78,148

|

17,570

|

—

|

—

|

—

|

—

|

95,718

|

|||||||||||||||

|

Preferred

dividends(6)

|

4,200

|

4,200

|

4,200

|

4,200

|

4,200

|

4,200

|

25,200

|

|||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||

|

Total

commitments

|

$

|

171,581

|

$

|

27,640

|

$

|

10,034

|

$

|

10,027

|

$

|

24,602

|

$

|

5,000

|

$

|

248,884

|

||||||||

| (1) |

Unconditional

purchase commitments for production materials incurred in the normal

course of business.

|

| (2) |

Under

Front Range’s three term loan agreements quarterly payments apply to

accrued interest and principal and mature in 2011, but have required

principal payments based on a ten year amortization schedule. Interest

fluctuates at a premium of 2.75-3.50% based on the 30- or 90-day

LIBOR,

depending on the loan. At December 31, 2006, the 30-day LIBOR was

5.33%

and the 90-day LIBOR was 5.32%.

|

| (3) |

The

water rights lease obligation of Front Range relates to a lease agreement

for water in production processes. The lease requires an initial

payment

of $400,000 and annual payments of $160,000 per year for the next

ten

years. The future payments were discounted using a 5.25% interest

rate.

|

| (4) |

Future

minimum payments under non cancellable operating

leases.

|

| (5) |

Construction

commitments for in-progress and contracted ethanol processing

facilities.

|

| (6) |

Represents

dividends on 5,250,000 shares of Series A Preferred

Stock.

|

|

Commodity

Derivatives

|

Interest

Rate Derivatives

|

||||||

|

Gain/(Loss)*

|

Gain/(Loss)*

|

||||||

|

Beginning

balance, January 1, 2006

|

$

|

—

|

$

|

—

|

|||

|

Net

changes

|

1,307

|

(272

|

)

|

||||

|

Less:

Amount reclassified to revenue

|

1,281

|

—

|

|||||

|

Less:

Amount reclassified to cost of goods sold

|

(435

|

)

|

—

|

||||

|

Less:

Amount reclassified to other income (expense)

|

—

|

(7

|

)

|

||||

|

Ending

balance, December 31, 2006

|

$

|

461

|

$

|

(265

|

)

|

||

|

2006

|

2005

|

||||||

|

Commodity

futures

|

$

|

329

|

$

|

—

|

|||

|

Interest

rate options

|

125

|

—

|

|||||

|

Total

|

$

|

454

|

$

|

—

|

|||

|

(i)

|

pertain

to the maintenance of records that, in reasonable detail, accurately

and

fairly reflect the transactions and dispositions of our

assets;

|

|

(ii)

|

provide

reasonable assurance that transactions are recorded as necessary

to permit

preparation of financial statements in accordance with generally

accepted

accounting principles, and that our receipts and expenditures are

being

made only in accordance with authorizations of our management and

directors; and

|

|

(iii)

|

provide

reasonable assurance regarding prevention or timely detection of

unauthorized acquisition, use or disposition of our assets that could

have

a material affect on our financial

statements.

|

|

(1)

|

We

had not effectively implemented comprehensive entity-level internal

controls.

|

|

(2)

|

We

did not have a sufficient complement of personnel with appropriate

training and experience in generally accepted accounting principals,

or

GAAP.

|

|

(3)

|

We

did not adequately segregate the duties of different personnel within

our

accounting group due to an insufficient complement of staff.

|

|

(4)

|

We

did not perform adequate oversight of certain accounting functions

and

maintained inadequate documentation of management review and approval

of

accounting transactions and financial reporting

processes.

|

|

(5)

|

We

did not have adequate controls governing major account invoice processing

and payment.

|

|

(6)

|

We

had not fully implemented certain control activities and capabilities

included in the design of our enterprise resource platform, or ERP,

system.

|

|

(7)

|

We

did not have adequate access and data and formulaic integrity controls

over critical spreadsheets used in connection with accounting and

financial reporting.

|

|

(1)

|

The

Company had not effectively implemented comprehensive entity-level

internal controls;

|

|

(2)

|

The

Company did not have a sufficient complement of personnel with appropriate

training and experience in generally accepted accounting principles,

or

GAAP;

|

|

(3)

|

The

Company did not adequately segregate the duties of different personnel

within its accounting group due to an insufficient complement of

staff;

|

|

(4)

|

The

Company did not perform adequate oversight of certain accounting

functions

and maintained inadequate documentation of management review and

approval

of accounting transactions and financial reporting

processes;

|

|

(5)

|

The

Company did not have adequate controls governing major account invoice

processing and payment;

|

|

(6)

|

The

Company did not fully implement certain control activities and

capabilities included in the design of its enterprise resource platform,

or ERP system; and

|

|

(7)

|

The

Company did not maintain adequate access and data and formulaic integrity

controls over critical spreadsheets used in connection with accounting

and

financial reporting.

|

|

Report

of Independent Registered Public Accounting Firm

|

F-2

|

|

Consolidated

Balance Sheets as of December 31, 2006 and 2005

|

F-3

|

|

Consolidated

Statements of Operations for the Years Ended December 31, 2006, 2005

and 2004

|

F-5

|

|

Consolidated

Statements of Comprehensive Income (Loss) for the Years Ended

December 31, 2006, 2005 and 2004

|

F-6

|

|

Consolidated

Statement of Stockholders’ Equity for the Years Ended December 31,

2006, 2005 and 2004

|

F-7

|

|

Consolidated

Statements of Cash Flows for the Years Ended December 31, 2006, 2005

and 2004

|

F-10

|

|

Notes

to Consolidated Financial Statements

|

F-12

|

|

December

31,

|

|||||||

|

ASSETS

|

2006

|

2005

|

|||||

|

Current

Assets:

|

|||||||

|

Cash

and cash equivalents

|

$

|

44,053

|

$

|

4,521

|

|||

|

Investments

in marketable securities

|

39,119

|

2,750

|

|||||

|

Accounts

receivable, net (including $1,188 and $938 as

of

December 31, 2006 and 2005,

respectively,

from a related party)

|

29,322

|

4,948

|

|||||

|

Restricted

cash

|

1,567

|

—

|

|||||

|

Notes

receivable - related party

|

—

|

136

|

|||||

|

Inventories

|

7,595

|

363

|

|||||

|

Prepaid

expenses

|

1,053

|

627

|

|||||

|

Prepaid

inventory

|

2,029

|

1,349

|

|||||

|

Other

current assets

|

2,307

|

86

|

|||||

|

Total

current assets

|

127,045

|

14,780

|

|||||

|

Property

and Equipment, Net

|

196,156

|

23,208

|

|||||

|

Other

Assets:

|

|||||||

|

Restricted

cash

|

24,851

|

—

|

|||||

|

Deposits

and advances

|

9,040

|

14

|

|||||

|

Goodwill

|

85,307

|

2,566

|

|||||

|

Intangible

assets, net

|

10,155

|

7,569

|

|||||

|

Other

assets

|

1,266

|

48

|

|||||

|

Total

other assets

|

130,619

|

10,197

|

|||||

|

Total

Assets

|

$

|

453,820

|

$

|

48,185

|

|||

|

December

31,

|

|||||||

|

LIABILITIES

AND STOCKHOLDERS’ EQUITY

|

2006

|

2005

|

|||||

|

Current

Liabilities:

|

|||||||

|

Current

portion - related party note payable

|

$

|

—

|

$

|

1,200

|

|||

|

Current

portion - notes payable

|

4,125

|

—

|

|||||

|

Accounts

payable - trade

|

11,483

|

4,755

|

|||||

|

Accounts

payable - related party

|

3,884

|

6,412

|

|||||

|

Accrued

retention - related party

|

5,538

|

1,450

|

|||||

|

Accrued

payroll

|

766

|

434

|

|||||

|

Other

accrued liabilities

|

4,798

|

3,423

|

|||||

|

Total

current liabilities

|

30,594

|

17,674

|

|||||

|

Related-party

notes payable, net of current portion

|

—

|

1,995

|

|||||

|

Notes

payable, net of current portion

|

28,970

|

—

|

|||||

|

Deferred

tax liability

|

1,091

|

—

|

|||||

|

Other

liabilities

|

357

|

—

|

|||||

|

Total

Liabilities

|

61,012

|

19,669

|

|||||

|

Commitments

and Contingencies (Notes 2, 9, 15, 16 and 18)

|

|||||||

|

Non-controlling

interest in variable interest entity

|

94,363

|

—

|

|||||

|

Stockholders’

Equity:

|

|||||||

|

Preferred

stock, $0.001 par value; 10,000 shares authorized; 5,250 and 0 shares

issued and outstanding as of December 31,

2006 and 2005, respectively

|

5

|

—

|

|||||

|

Common

stock, $0.001 par value; 100,000 shares authorized; 40,269 and 28,874

shares issued and outstanding as of December 31, 2006 and 2005,

respectively

|

40

|

29

|

|||||

|

Additional

paid-in capital

|

397,535

|

42,071

|

|||||

|

Other

comprehensive income

|

545

|

—

|

|||||

|

Accumulated

deficit

|

(99,680

|

)

|

(13,584

|

)

|

|||

|

Total

stockholders’ equity

|

298,445

|

28,516

|

|||||

|

Total

Liabilities and Stockholders’ Equity

|

$

|

453,820

|

$

|

48,185

|

|||

|

Years

Ended December 31,

|

||||||||||

|

2006

|

2005

|

2004

|

||||||||

|

Net

sales (including $16,985, $9,060, and $0 for the years ended

December 31, 2006, 2005 and 2004, respectively, to a related

party)

|

$

|

226,356

|

$

|

87,599

|

$

|

20

|

||||

|

Cost

of goods sold

|

201,527

|

84,444

|

13

|

|||||||

|

Gross

profit

|

24,829

|

3,155

|

7

|

|||||||

|

Selling,

general and administrative expenses

|

24,641

|

12,638

|

2,277

|

|||||||

|

Income

(loss) from operations

|

188

|

(9,483

|

)

|

(2,270

|

)

|

|||||

|

Other

income (expense), net

|

3,426

|

(440

|

)

|

(532

|

)

|

|||||

|

Income

(loss) before provision for income taxes and non-controlling interest

in

variable interest entity

|

3,614

|

(9,923

|

)

|

(2,802

|

)

|

|||||

|

Provision

for income taxes

|

—

|

—

|

—

|

|||||||

|

Income

(loss) before non-controlling interest in variable interest entity

|

3,614

|

(9,923

|

)

|

(2,802

|

)

|

|||||

|

Non-controlling

interest in variable interest entity

|

(3,756

|

)

|

—

|

—

|

||||||

|

Net

loss

|

$

|

(142

|

)

|

$

|

(9,923

|

)

|

$

|

(2,802

|

)

|

|

|

Preferred

stock dividends

|

$

|

(2,998

|

)

|

$

|

—

|

$

|

—

|

|||

|

Deemed

dividend on preferred stock

|

(84,000

|

)

|

—

|

—

|

||||||

|

Loss

available to common stockholders

|

$

|

(87,140

|

)

|

$

|

(9,923

|

)

|

$

|

(2,802

|

)

|

|

|

Net

loss per share, basic and diluted

|

$

|

(2.50

|

)

|

$

|

(0.40

|

)

|

$

|

(0.23

|

)

|

|

|

Weighted-average

shares outstanding, basic and diluted

|

34,855

|

25,066

|

12,397

|

|||||||

|

For

the Years Ended December 31,

|

||||||||||

|

2006

|

2005

|

2004

|

||||||||

|

Net

loss

|

$

|

(142

|

)

|

$

|

(9,923

|

)

|

$

|

(2,802

|

)

|

|

|

Other

comprehensive income, net of tax:

|

||||||||||

|

Cash

flow hedges:

|

||||||||||

|

Net

change in the fair value of derivatives, net of tax

|

196

|

—

|

—

|

|||||||

|

Unrealized

gain on restricted available-for-sale securities

|

349

|

—

|

—

|

|||||||

|

Comprehensive

income (loss)

|

$

|

403

|

$

|

(9,923

|

)

|

$

|

(2,802

|

)

|

||

|

Preferred

Stock

|

Common

Stock

|

Additional

Paid-In

Capital

|

Other

Compre-

hensive

Income

|

Accumulated

Deficit

|

Total

|

||||||||||||||||||||

|

Shares

|

Amount

|

Shares

|

Amount

|

||||||||||||||||||||||

|

Balances,

January 1, 2004

|

—

|

$

|

—

|

11,733

|

$

|

12

|

$

|

2,215

|

$

|

—

|

$

|

(859

|

)

|

$

|

1,368

|

||||||||||

|

Issuance

of common stock to friends and family, net of offering costs of

$7

|

—

|

—

|

19

|

—

|

21

|

—

|

—

|

21

|

|||||||||||||||||

|

Issuance

of warrants to purchase 920 shares of common stock for non-cash

compensation to non-employee for services

|

—

|

—

|

—

|

—

|

1,380

|

—

|

—

|

1,380

|

|||||||||||||||||

|

Exercise

of warrants

|

—

|

—

|

920

|

1

|

(1

|

)

|

—

|

—

|

—

|

||||||||||||||||

|

Issuance

of common stock in working capital round, net of offering costs

of $107

|

—

|

—

|

500

|

—

|

825

|

—

|

—

|

825

|

|||||||||||||||||

|

Issuance

of common stock in working capital round, net of offering costs

of

$2

|

—

|

—

|

104

|

—

|

309

|

—

|

—

|

309

|

|||||||||||||||||

|

Conversion

of LDI debt

|

—

|

—

|

170

|

—

|

255

|

—

|

—

|

255

|

|||||||||||||||||

|

Comprehensive

loss

|

—

|

—

|

—

|

—

|

—

|

—

|

(2,802

|

)

|

(2,802

|

)

|

|||||||||||||||

|

Balances,

December 31, 2004

|

—

|

$

|

—

|

13,446

|

$

|

13

|

$

|

5,004

|

$

|

—

|

$

|

(3,661

|

)

|

$

|

1,356

|

||||||||||

|

Preferred

Stock

|

Common

Stock

|

Additional

Paid-In

Capital

|

Other

Compre-

hensive

Income

|

Accumulated

Deficit

|

Total

|

||||||||||||||||||||

|

Shares

|

Amount

|

Shares

|

Amount

|

||||||||||||||||||||||

|

Balances,

January 1, 2005

|

—

|

—

|

13,446

|

$

|

13

|

$

|

5,004

|

$

|

—

|

$

|

(3,661

|

)

|

$

|

1,356

|

|||||||||||

|

Amounts

received from shareholder

|

—

|

—

|

—

|

—

|

67

|

—

|

—

|

67

|

|||||||||||||||||

|

Issuance

of shares in private placement, net of offering costs of

$2,125

|

—

|

—

|

7,000

|

7

|

18,868

|

—

|

—

|

18,875

|

|||||||||||||||||

|

Share

Exchange

|

—

|

—

|

7,090

|

7

|

13,577

|

—

|

—

|

13,584

|

|||||||||||||||||

|

Acquisition

costs in excess of cash acquired

|

—

|

—

|

—

|

—

|

481

|

—

|

—

|

481

|

|||||||||||||||||

|

Compensation

expense related to issuance of warrants for consulting

services

|

—

|

—

|

—

|

—

|

927

|

—

|

—

|

927

|

|||||||||||||||||

|

Stock

issued for exercise of warrants for cash

|

—

|

—

|

237

|

—

|

490

|

—

|

—

|

490

|

|||||||||||||||||

|

Stock

issued in cashless exercise of warrants

|

—

|

—

|

34

|

—

|

—

|

—

|

—

|

—

|

|||||||||||||||||

|

Compensation

expense for options issued to employees

|

—

|

—

|

—

|

—

|

80

|

—

|

—

|

80

|

|||||||||||||||||

|

Compensation

expense for employee option converted into a warrant

|

—

|

—

|

—

|

—

|

233

|

—

|

—

|

233

|

|||||||||||||||||

|

Stock

issued for exercise of stock options for cash

|

—

|

—

|

78

|

—

|

450

|

—

|

—

|

450

|

|||||||||||||||||

|

Stock

issued for cashless exercise of stock options

|

—

|

—

|

89

|

1

|

(1

|

)

|

—

|

—

|

—

|

||||||||||||||||

|

Issuance

of stock to employees

|

—

|

—

|

70

|

—

|

651

|

—

|

—

|

651

|

|||||||||||||||||

|

Conversion

of LDI debt

|

—

|

—

|

830

|

1

|

1,244

|

—

|

—

|

1,245

|

|||||||||||||||||

|

Comprehensive

loss

|

—

|

—

|

—

|

—

|

—

|

—

|

(9,923

|

)

|

(9,923

|

)

|

|||||||||||||||

|

Balances,

December 31, 2005

|

—

|

$

|

—

|

28,874

|

$

|

29

|

$

|

42,071

|

$

|

—

|

$

|

(13,584

|

)

|

$

|

28,516

|

||||||||||

|

Preferred

Stock

|

Common

Stock

|

Additional

Paid-In

Capital

|

Other

Compre-

hensive

Income

|

Accumulated

Deficit

|

Total

|

||||||||||||||||||||

|

Shares

|

Amount

|

Shares

|

Amount

|

||||||||||||||||||||||

|

Balances,

January 1, 2006

|

—

|

$

|

—

|

28,874

|

$

|

29

|

$

|

42,071

|

$

|

—

|

$

|

(13,584

|

)

|

$

|

28,516

|

||||||||||

|

Cumulative

effect adjustment (Note 11)

|

—

|

—

|

—

|

—

|

—

|

—

|

1,043

|

1,043

|

|||||||||||||||||

|

Issuance

of preferred stock, net of offering costs of $1,434

|

5,250

|

5

|

—

|

—

|

82,561

|

—

|

—

|

82,566

|

|||||||||||||||||

|

Beneficial

conversion feature on issuance of preferred stock and preferred

dividend

declared

|

—

|

—

|

—

|

—

|

84,000

|

—

|

(86,998

|

)

|

(2,998

|

)

|

|||||||||||||||

|

Issuance

of common stock for private investment in public equity, net of

offering

costs of $7,381

|

—

|

—

|

5,497

|

5

|

137,614

|

—

|

—

|

137,619

|

|||||||||||||||||

|

Exercise

of warrants and Accessity options

|

—

|

—

|

71

|

—

|

89

|

—

|

—

|

89

|

|||||||||||||||||

|

Share-based

compensation expense - restricted stock to employees and

directors

|

—

|

—

|

894

|

1

|

3,047

|

—

|

—

|

3,048

|

|||||||||||||||||

|

Common

stock issued for purchase of 42% interest in Front Range

|

—

|

—

|

2,082

|

2

|

30,006

|

—

|

—

|

30,008

|

|||||||||||||||||

|

Fair

value of warrants issued for purchase of 42% interest in Front

Range

|

—

|

—

|

—

|

—

|

5,087

|

—

|

—

|

5,087

|

|||||||||||||||||

|

Collection

of stockholder receivable

|

—

|

—

|

—

|

—

|

1

|

—

|

—

|

1

|

|||||||||||||||||

|

Share-based

compensation expense - options and warrants to employees and

consultants

|

—

|

—

|

—

|

—

|

3,201

|

—

|

—

|

3,201

|

|||||||||||||||||

|

Stock

issued for exercise of warrants for cash

|

—

|

—

|

2,518

|

3

|

8,556

|

—

|

—

|

8,559

|

|||||||||||||||||

|

Stock

issued in cashless exercise of warrants

|

—

|

—

|

150

|

—

|

—

|

—

|

—

|

—

|

|||||||||||||||||

|

Stock

issued for exercise of stock options for cash

|

—

|

—

|

183

|

—

|

1,303

|

—

|

—

|

1,303

|

|||||||||||||||||

|

Comprehensive

income

|

—

|

—

|

—

|

—

|

—

|

545

|

(142

|

)

|

403

|

||||||||||||||||

|

Balances,

December 31, 2006

|

5,250

|

$

|

5

|

40,269

|

$

|

40

|

$

|

397,536

|

$

|

545

|

$

|

(99,681

|

)

|

$

|

298,445

|

||||||||||

|

For

the Years Ended December 31,

|

||||||||||

|

2006

|

2005

|

2004

|

||||||||

|

Operating

Activities:

|

||||||||||

|

Net

loss

|

$

|

(142

|

)

|

$

|

(9,923

|

)

|

$

|

(2,802

|

)

|

|

|

Adjustments

to reconcile net loss to cash

provided by (used in) operating activities:

|

||||||||||

|

Depreciation

and amortization of intangibles

|

3,998

|

766

|

79

|

|||||||

|

Amortization

of deferred financing fees

|

1,069

|

21

|

20

|

|||||||

|

Interest

expense relating to amortization of debt discount

|

404

|

428

|

240

|

|||||||

|

Discontinued

design of cogeneration facility

|

—

|

311

|

—

|

|||||||

|

Non-cash

compensation expense

|

4,466

|

963

|

—

|

|||||||

|

Non-cash

consulting expense

|

1,782

|

1,099

|

1,207

|

|||||||

|

Expiration

of option acquired in acquisition of ReEnergy

|

—

|

120

|

—

|

|||||||

|

Feasibility

study expensed in connection with acquisition of ReEnergy

|

—

|

852

|

—

|

|||||||

|

Acquisition

cost expense in excess of cash received

|

—

|

481

|

—

|

|||||||

|

Gain/loss

on cash flow hedges

|

162

|

—

|

—

|

|||||||

|

Non-controlling

interest in variable interest entity

|

3,756

|

—

|

—

|

|||||||

|

Bad

debt expense

|

83

|

—

|

—

|

|||||||

|

Changes

in operating assets and liabilities:

|

—

|

|||||||||

|

Accounts

receivable

|

(20,939

|

)

|

(2,427

|

)

|

15

|

|||||

|

Increase

in restricted cash

|

(1,570

|

)

|

—

|

—

|

||||||

|

Notes

receivable, related party

|

136

|

(131

|

)

|

(5

|

)

|

|||||

|

Inventories

|

(3,697

|

)

|

219

|

2

|

||||||

|

Prepaid

expenses and other assets

|

(1,030

|

)

|

(515

|

)

|

(99

|

)

|

||||

|

Prepaid

inventory

|

(679

|

)

|

(1,042

|

)

|

—

|

|||||

|

Other

receivable

|

—

|

(22

|

)

|

263

|

||||||

|

Accounts

payable and accrued expenses

|

2,498

|

7,242

|

250

|

|||||||

|

Accounts

payable, and accrued expenses (related party)

|

1,559

|

5,565

|

396

|

|||||||

|

Net

cash provided by (used in) operating activities

|

(8,144

|

)

|

4,007

|

(434

|

)

|

|||||

|

Investing

Activities:

|

||||||||||

|

Additions

to property and equipment

|

(82,454

|

)

|

(17,273

|

)

|

(740

|

)

|

||||

|

Advances

on equipment

|

(9,041

|

)

|

—

|

—

|

||||||

|

Proceeds

from sales of available-for-sale investments

|

—

|

12,250

|

—

|

|||||||

|

Purchases

of available-for-sale investments

|

(28,962

|

)

|

(15,000

|

)

|

—

|

|||||

|

Payment

on deposit

|

—

|

(14

|

)

|

—

|

||||||

|

Net

cash acquired in acquisition of Kinergy, ReEnergy and

Accessity

|

—

|

3,327

|

—

|

|||||||

|

Cash

payments in connection with share exchange transaction

|

—

|

(541

|

)

|

(430

|

)

|

|||||

|

Payments

received on related party note receivable

|

—

|

—

|

200

|

|||||||

|

Acquisition

of 42% interest in Front Range, net of cash received

|

(29,514

|

)

|

—

|

—

|

||||||

|

Increase

in restricted cash designated for construction projects

|

(24,851

|

)

|

—

|

—

|

||||||

|

Net

cash used in investing activities

|

(174,822

|

)

|

(17,251

|

)

|

(970

|

)

|

||||

|

For

the Years Ended December 31,

|

||||||||||

|

2006

|

2005

|

2004

|

||||||||

|

Financing

Activities:

|

||||||||||

|

Proceeds

from sale of common stock, net

|

137,619

|

18,875

|

1,155

|

|||||||

|

Proceeds

from sale of preferred stock, net

|

82,566

|

—

|

—

|

|||||||

|

Payment

on notes payable, Kinergy and ReEnergy

|

—

|

(2,097

|

)

|

—

|

||||||

|

Proceeds

from notes payable, related party

|

—

|

280

|

—

|

|||||||

|

Payment

on notes payable, related party

|

—

|

(300

|

)

|

—

|

||||||

|

Proceeds

from exercise of warrants and stock options

|

9,951

|

939

|

—

|

|||||||

|

Principal

payments paid on borrowings

|

(1,005

|

)

|

—

|

—

|

||||||

|

Principal

payments paid on borrowings (related party)

|

(3,600

|

)

|

—

|

—

|

||||||

|

Cash

paid for debt issuance costs

|

(3,036

|

)

|

—

|

—

|

||||||

|

Proceeds

from borrowing

|

1,950

|

—

|

—

|

|||||||

|

Preferred

share dividend paid

|

(1,948

|

)

|

—

|

—

|

||||||

|

Receipt

of stockholder receivable

|

1

|

68

|

—

|

|||||||

|

Net

cash provided by financing activities

|

222,498

|

17,765

|

1,155

|

|||||||

|

Net

increase in cash and cash equivalents

|

39,532

|

4,521

|

(249

|

)

|

||||||

|

Cash

and cash equivalents at beginning of period

|

4,521

|

—

|

249

|

|||||||

|

Cash

and cash equivalents at end of period

|

$

|

44,053

|

$

|

4,521

|

—

|

|||||

|

Supplemental

Information:

|

||||||||||

|

Interest

paid

|

$

|

966

|

$

|

387

|

$

|

422

|

||||

|

Non-Cash

Financing and Investing activities:

|

||||||||||

|

Change

in fair value of derivative instruments

|

$

|

196

|

$

|

—

|

$

|

—

|

||||

|

Preferred

stock dividend declared

|

$

|

1,050

|

$

|

—

|

$

|

—

|

||||

|

Deemed

dividend on preferred stock (Note 14)

|

$

|

84,000

|

$

|

—

|

$

|

—

|

||||

|

Unrealized

gain on restricted available-for-sale securities

|

$

|

349

|

$

|

—

|

$

|

—

|

||||

|

Transaction

costs associated with acquisition of 42% interest in Front

Range

|

$

|

304

|

$

|

—

|

$

|

—

|

||||

|

Issuance

of common stock associated with acquisition of 42% interest in Front

Range

|

$

|

30,008

|

$

|

—

|

$

|

—

|

||||

|

Issuance

of warrant associated with acquisition of 42% interest in Front

Range

|

$

|

5,087

|

$

|

—

|

$

|

—

|

||||

|

Cumulative

effect adjustment (Note 11)

|

$

|

2,134

|

$

|

—

|

$

|

—

|

||||

|

Conversion

of debt to equity

|

$

|

—

|

$

|

1,245

|

$

|

255

|

||||

|

Issuance

of stock for receivable

|

$

|

—

|

$

|

—

|

$

|

67

|

||||

|

Purchase

of ReEnergy with stock

|

$

|

—

|

$

|

316

|

$

|

—

|

||||

|

Shares

contributed by stockholder in purchase of ReEnergy

|

$

|

—

|

$

|

506

|

$

|

—

|

||||

|

Shares

contributed by stockholder in purchase of Kinergy

|

$

|

—

|

$

|

1,012

|

$

|

—

|

||||

|

Purchase

of Kinergy with stock

|

$

|

—

|

$

|

9,804

|

$

|

—

|

||||

|

1.

|

ORGANIZATION,

SIGNIFICANT ACCOUNTING POLICIES

AND RECENT ACCOUNTING

PRONOUNCEMENTS.

|

|

2006

|

2005

|

2004

|

|||

|

Customer

A

|

13%

|

18%

|

0%

|

||

|

Customer

B

|

12%

|

11%

|

0%

|

||

|

Customer

C

|

8%

|

10%

|

0%

|

||

|

Customer

D

|

0%

|

0%

|

36%

|

||

|

Customer

E

|

0%

|

0%

|

25%

|

||

|

Customer

F

|

0%

|

0%

|

22%

|

||

|

Customer

G

|

0%

|

0%

|

15%

|

|

2006

|

2005

|

2004

|

|||

|

Supplier

A

|

17%

|

22%

|

0%

|

||

|

Supplier

B

|

5%

|

20%

|

0%

|

||

|

Supplier

C

|

11%

|

17%

|

0%

|

||

|

Supplier

D

|

22%

|

9%

|

0%

|

|

2006

|

2005

|

||||||

|

Raw

materials

|

$

|

3,709

|

$

|

—

|

|||

|

Work

in progress

|

873

|

—

|

|||||

|

Finished

goods

|

2,452

|

—

|

|||||

|

Other

|

561

|

363

|

|||||

|

Total

|

$

|

7,595

|

$

|

363

|

|||

|

Buildings

|

40

years

|

|

Site

improvements and utilities

|

25

years

|

|

Facilities

and plant equipment

|

10

- 25 years

|

|

Other

equipment and vehicles

|

7

-

10 years

|

|

Office

furniture, fixtures and equipment

|

5

-

10 years

|

|

Water

rights

|

99

years

|

|

Year

Ended December 31,

|

||||||||||

|

2006

|

2005